The Global Reagent Squeeze: Supply Chain Vulnerabilities in Critical Mineral Processing

Why global Mining Equity Valuation Assumptions Are about to be Turned Upside Down

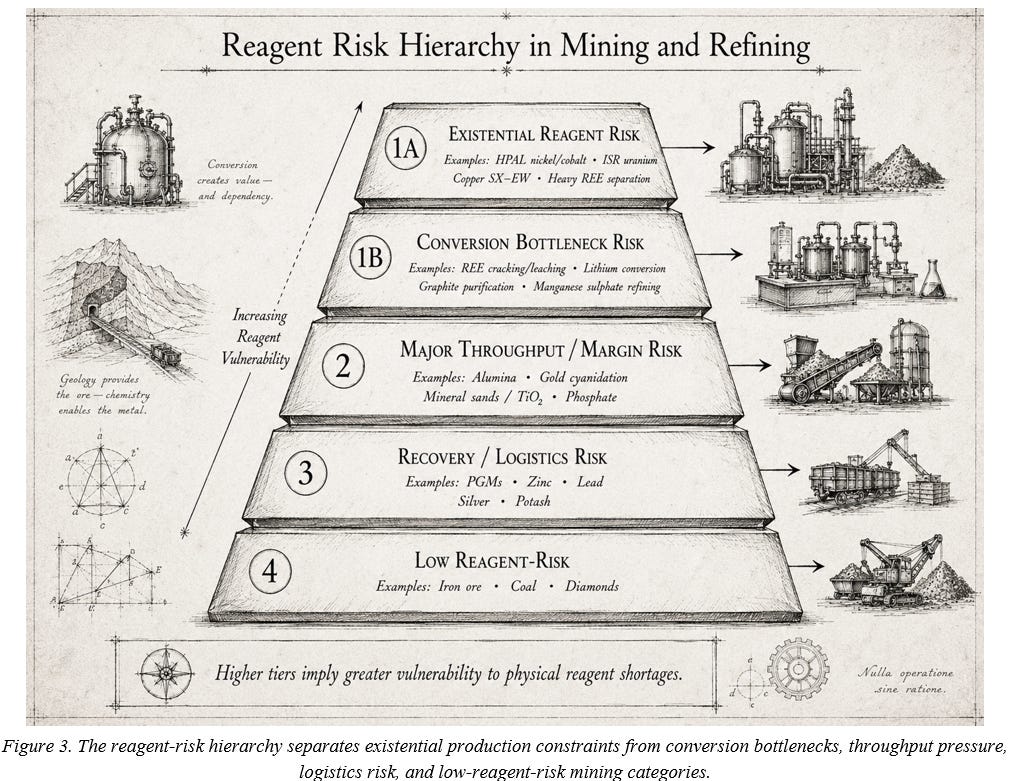

1. Introduction: The Invisible Constriction

The global transition toward electrification, renewable energy infrastructure, and advanced defence technologies has historically been analysed predominantly through the lens of geological scarcity.

Market forecasts, geopolitical strategies, and corporate risk assessments have focused intensively on the availability of physical reserves of copper, nickel, lithium, rare-earth elements, and uranium. International

However, the cascading geopolitical industrial events of 2025 and early 2026 have exposed a flaw in this traditional analytical framework: the severe vulnerability of the critical minerals sector lies in the reliable availability of the highly specific chemical reagents required to process it into refined metal

The mining industry is witnessing an accelerated structural shift from geological scarcity to chemical input bottlenecks, where the architecture of modern metallurgy is being severely constrained by the geopolitical and logistical realities of the global reagent supply chain.

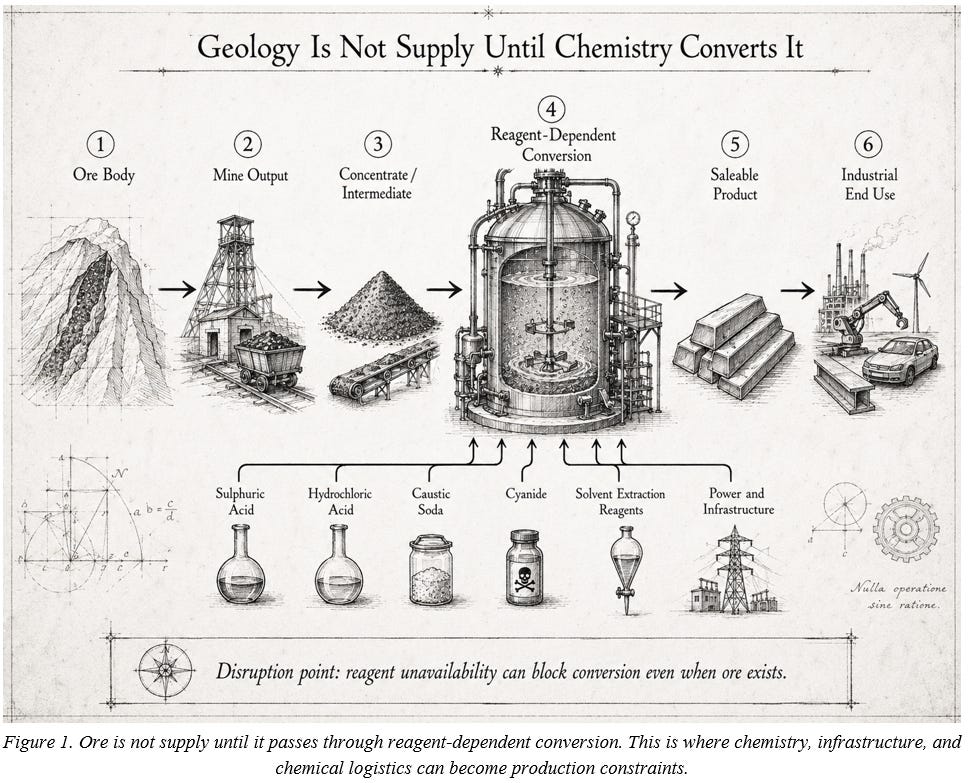

Modern mineral processing relies on highly specialised hydrometallurgical and physiochemical techniques.

Processes such as solvent extraction and electrowinning (SX-EW) for copper oxide ores, high-pressure acid leaching (HPAL) for lateritic nickel, and in-situ recovery (ISR) for uranium demand vast, continuous volumes of high-purity sulphuric acid

Furthermore, the separation of rare earth elements requires precise, multi-stage applications of specialised organophosphorus solvent extractants, while primary gold extraction remains dependent on the supply of sodium cyanide

As global ore grades steadily decline, copper ore grades alone have fallen by approximately 40% since 1991. Mining operations are forced to process exponentially more waste rock to yield the same volume of target metal.

This lower grades increases reagent consumption per tonne of finished product, tightening the industry’s dependence on chemical manufacturers.

While we readily understand that we need many inputs to manufacture a product, we fail to see a similar process in the production of our finished metals.

The Metals-versus-Food Paradox

The central paradox of our age is now impossible to ignore.

The global transition to electrification, renewable energy infrastructure, and advanced defence technologies was intended to free humanity from dependence on fossil fuels.

Yet the chemical reagents that make this transition possible are not new green inventions; they are direct by-products of the fossil-fuel economy itself. And today these same reagents have become the arena for an unforgiving contest between two of civilisation’s most basic imperatives: feeding eight billion people and powering the electrified world.

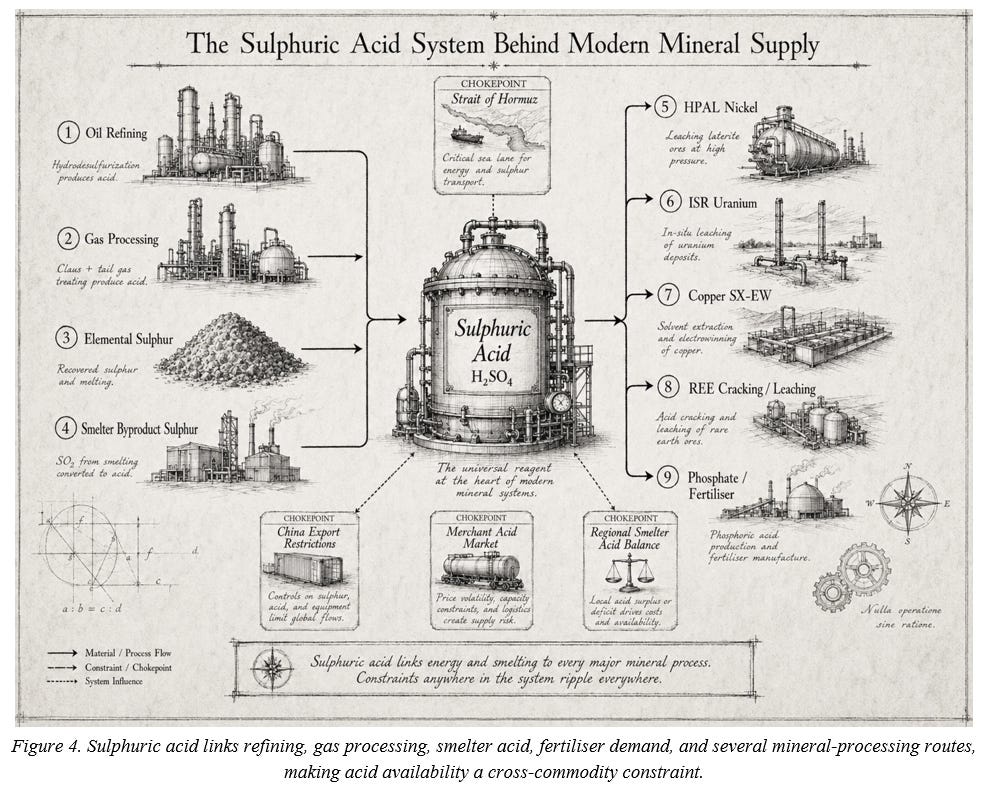

The molecule at the heart of the conflict is sulphuric acid. It is the single most important chemical input for almost every major hydrometallurgical process in modern mining.

It leaches copper from oxide ores in Chile and Africa, dissolves nickel and cobalt from laterite deposits in Indonesia, extracts uranium in Kazakhstan, and separates rare-earth elements.

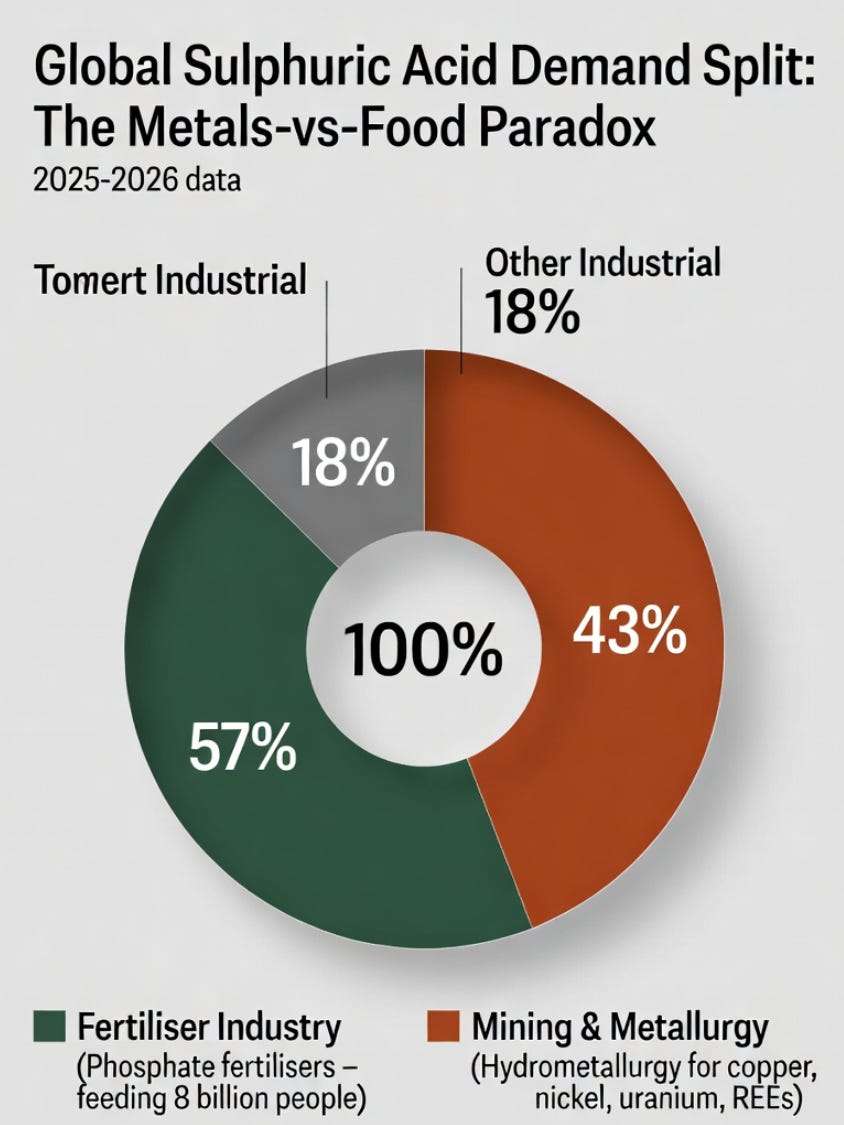

At the same time, sulphuric acid is the primary feedstock used to convert phosphate rock into phosphate fertilisers, the nutrients that sustain global agriculture. More than half of all sulphuric acid produced on Earth (55–60 %) is consumed by the fertiliser industry. Mining, even at the peak intensity required by the energy transition, accounts for only a fraction of total demand.

This creates a direct, molecule-for-molecule competition. Every extra tonne of copper cathode, nickel mixed hydroxide precipitate, or uranium yellowcake produced through acid-intensive methods consumes acid that could otherwise have been used to make fertiliser.

The dual shocks of 2026, the effective closure of the Strait of Hormuz to elemental sulphur shipments and China’s comprehensive ban on sulphuric acid exports have turned this latent competition into an immediate, zero-sum geopolitical triage.

Governments facing hungry populations have already begun choosing food security over metal security. To make it even more complicated, governments may have to choose between food and defence. Weapons and green energy manufacturers use the same reagents as herbicides, fertilisers and pesticide manufacturers.

Export controls in Zambia, domestic redirection of acid in Indonesia, and internal prioritisation orders in Chile are no longer exceptions; they are the new operating reality. When fertiliser prices surge 40–70 %, and crop-yield forecasts fall, political leaders make the same ancient choice: they feed their people first.

This is the deeper tragedy of our moment. In our urgent drive to decarbonise and escape fossil fuels, we have deepened our dependence on the chemical supply chains the fossil economy created, supply chains that great-power competition can now weaponise at will.

Geological scarcity of metals was always a technical problem that could, in theory, be solved. The contest between metals and food is a profound civilisational dilemma. The invisible constriction is no longer confined to remote mine sites. It is now written in the stark arithmetic of calories versus kilowatt-hours.

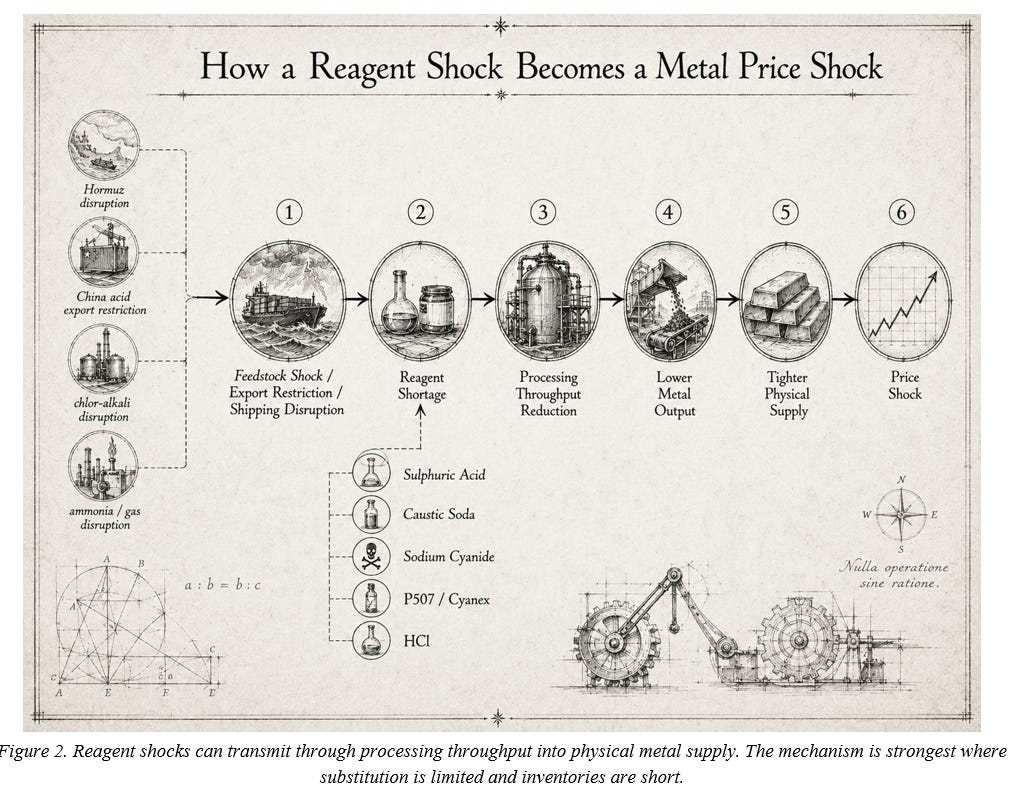

This vulnerability has been activated by two converging geopolitical shocks in the first half of 2026.

First, the closure of the Strait of Hormuz to commercial shipping severed the primary artery for global elemental sulphur trade, paralysing a supply chain that originates predominantly in Middle Eastern hydrocarbon refineries

Second, China implemented a comprehensive export ban on by-product sulphuric acid, seeking to ringfence domestic supply for its own agricultural and industrial sectors

Together, these events have orchestrated a dual supply shock that is about to choke the operations of base metal, precious metal, and battery material producers in their most critical chemical inputs.

The crisis is redefining the cost curves of global mining, triggering production downgrades, and proving conclusively that resource security cannot be achieved without integrated chemical supply chain resilience.

2. The Catalyst: Strait of Hormuz and the Sulphur Shock

Elemental sulphur is the foundational feedstock for the vast majority of global sulphuric acid production.

Unlike most mined commodities, sulphur is rarely extracted as a primary resource; rather, it is a compulsory byproduct recovered during the desulphurization of crude oil and the sweetening of sour natural gas, mandated by stringent environmental emissions standards

Because it is a byproduct of hydrocarbon refining, global sulphur production, which reached approximately 83.87 million metric tons in 2025, cannot be elastically scaled up on demand in response to rising price signals from the mining or agricultural sectors.

The critical vulnerability of this global market is its extreme geographic concentration.

The Middle East accounts for approximately 24% of total global sulphur production, but critically, the region controls roughly 50% of the world’s seaborne sulphur trade

Major processing facilities in Saudi Arabia (such as Jubail), the United Arab Emirates (Ruwais), and Qatar dominate international export volumes.

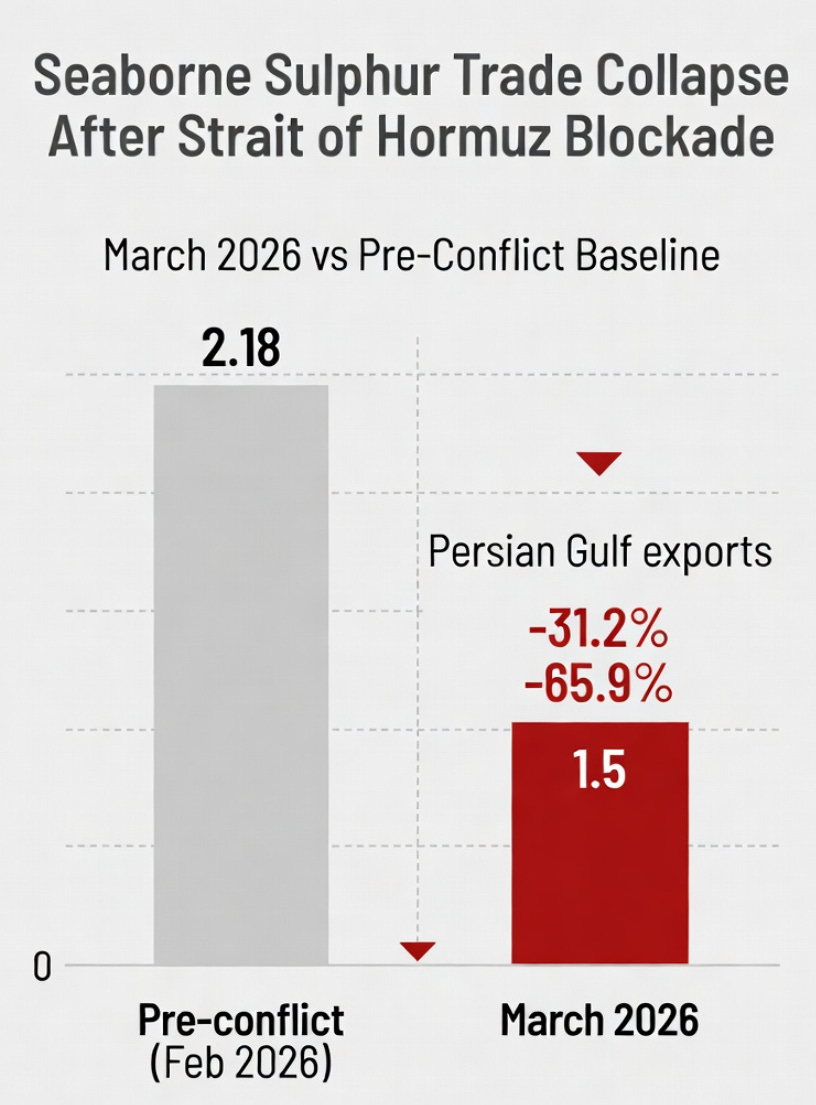

Consequently, the commercial blockade and escalating security risks in the Strait of Hormuz, initiated by the conflict involving Iran in late February 2026, effectively paralysed the world’s primary sulphur export artery.

The maritime disruption led to a large contraction in global trade. In March 2026 alone, global sulphur loadings onto dry bulk carriers collapsed by an estimated 31.2% month-on-month, falling to just 1.5 million tonnes

Export volumes in the Persian Gulf plummeted by nearly 65.9% in a single month. Because approximately 90% of ocean sulphur cargoes are transported on geared tonnage, specifically Handysize, Supramax, and Ultramax vessels, this segment has been disproportionately impacted by war-risk insurance premiums and route diversions.

The price response for spot sulphur prices delivered to the Mediterranean surged from ~ $155 per metric ton to over ~$400 per metric ton

In Asia, delivered prices into Indonesia spiked past $800 per metric ton, with some cargoes clearing as high as $1,000 per metric ton, compared to pre-conflict baselines of ~$500

For the mining industry, which relies on consistent, high-volume deliveries of elemental sulphur to feed acid-burning plants located at remote mine sites, this represents a supply shock. Mining operations can’t pivot to alternative feedstocks quickly; establishing new supply lines from North America or an alternative European refinery byproducts carries logistics premiums of $80 to $150 per metric ton.

3. The Multiplier: China’s Sulphuric Acid Export Ban

If the Strait of Hormuz blockade constrained the upstream supply of elemental sulphur, policy actions by China simultaneously suffocated the downstream supply of refined sulphuric acid.

China is the world’s largest producer and exporter of sulphuric acid, generating ~120 million tons annually against a total capacity of 141 million tons

In 2025, Chinese exports of chemicals surged by 73% year-on-year to reach 4.65 million tonnes, establishing the nation as the vital balancing mechanism for global acid

However, China’s vast domestic phosphate fertiliser industry, which accounts for the majority of internal acid consumption, competes directly with the export market.

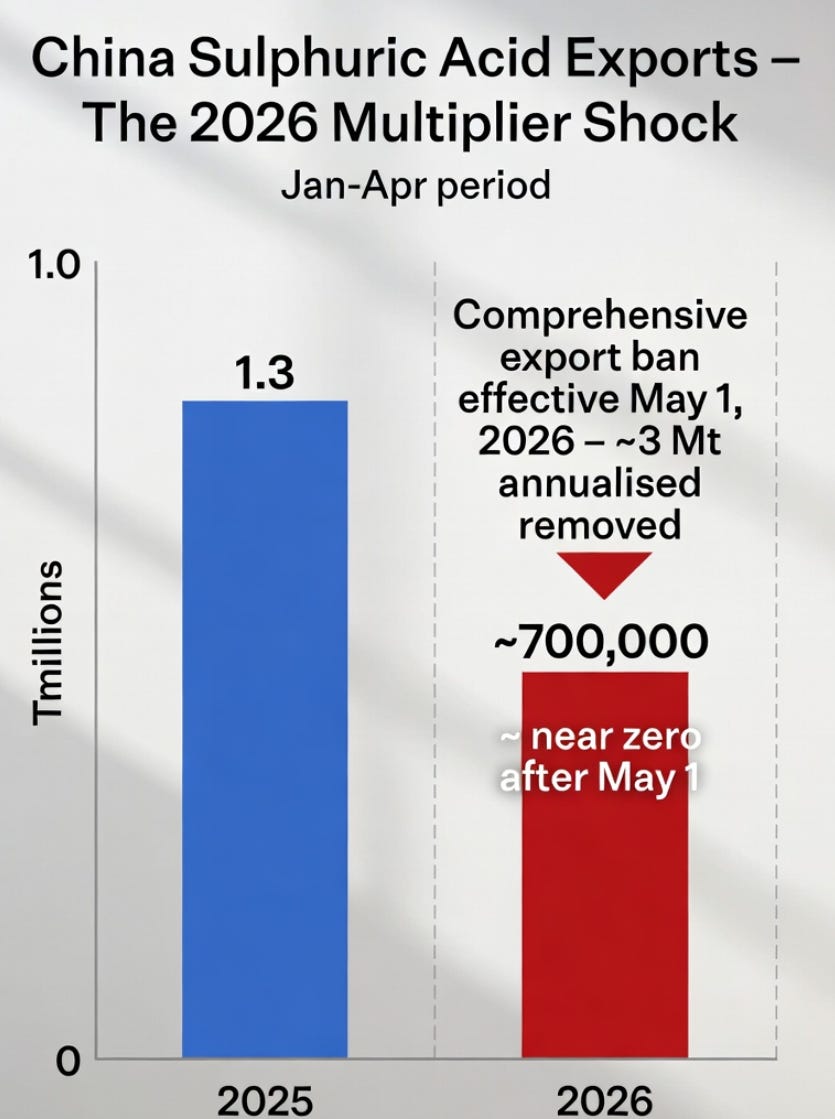

Faced with soaring global sulphur prices and the imperative to secure domestic food production ahead of the spring planting season, Beijing intervened aggressively. In early 2026, the National Development and Reform Commission implemented strict export quotas, limiting January-to-April outbound shipments to just 700,000 tonnes, a precipitous drop from the 1.3 million tonnes exported during the same period in 2025

This quota was quickly followed by a comprehensive export ban on by-product sulphuric acid, which took effect on May 1, 2026. The removal of nearly 3 million annualised tonnes from the seaborne market cannot be seamlessly replaced by other regional producers. It’s also the velocity of the change that wrongfoots users, faced with almost-instantaneous shortages in logistics that take time to resolve.

While Japan, South Korea, and India collectively possess some excess capacity, their combined ability to increase exports is estimated at a mere 500,000 tonnes, falling vastly short of the deficit created by China’s sudden withdrawal

This sudden policy shift operates as a crisis multiplier for the global mining sector.

The vast majority of China’s exported acid is generated as a byproduct of its massive domestic copper and zinc smelting industries. By trapping this acid within its borders, China forces international mining operations, particularly in Latin America and Africa, into a hyper-competitive spot market, where agricultural and industrial buyers bid up prices for dwindling global inventory.

This dynamic has severed traditional trade flows, leaving operations that rely on merchant acid procurement dangerously exposed to margin collapse.

4. The Structural Shift in Base Metal Economics

The convergence of the Hormuz sulphur shock and the Chinese acid ban is rewriting the economics of base metal extraction.

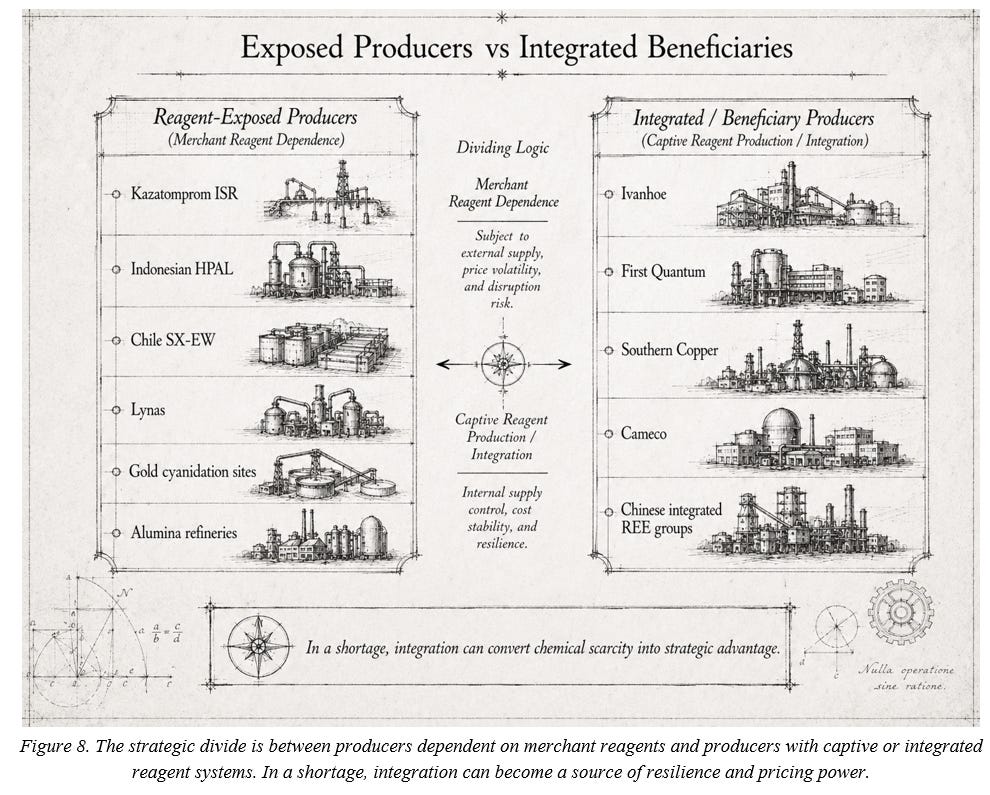

The crisis highlights a critical distinction in modern mining resilience: the divergence between pyrometallurgical and hydrometallurgical processing routes.

Operations that mine sulphide ores and process them through traditional smelting possess an inherent “natural hedge.” The smelting of sulphide concentrates produces sulphur dioxide gas, which is captured and converted into sulphuric acid on-site

These integrated facilities generate byproduct acid, partially insulating them from the global supply squeeze, and occasionally allowing them to profit as merchant sellers.

For example, Ivanhoe Mines’ Kamoa-Kakula complex in the DRC operates an on-site smelter that produces 1,350 tonnes of high-strength sulphuric acid per day, creating a highly lucrative byproduct credit that drastically lowers its C1 cash costs to $2.58/lb of copper. Ivanhoe Mines, “Ivanhoe Mines Issues 2026 First Quarter Financial Results,” May 6, 2026.

Conversely, operations exploiting oxide ores or complex laterites through hydrometallurgical leaching are entirely dependent on massive external reagent inputs. As ore grades decline globally, the reliance on acid-intensive leaching to extract economic value from marginal deposits has increased substantially.

This structural reliance has transformed sulphuric acid from a low-profile, background consumable into the primary rate-limiting factor for global metal production

The financial transmission mechanism is highly compressed; a delay in sulphur shipments from the Middle East directly reduces acid availability at the leach pad within weeks, compressing quarterly output and immediately impacting producer earnings independently of the spot price

The cost curve for global copper and nickel production has shifted upward, permanently altering the baseline economics of the energy transition.

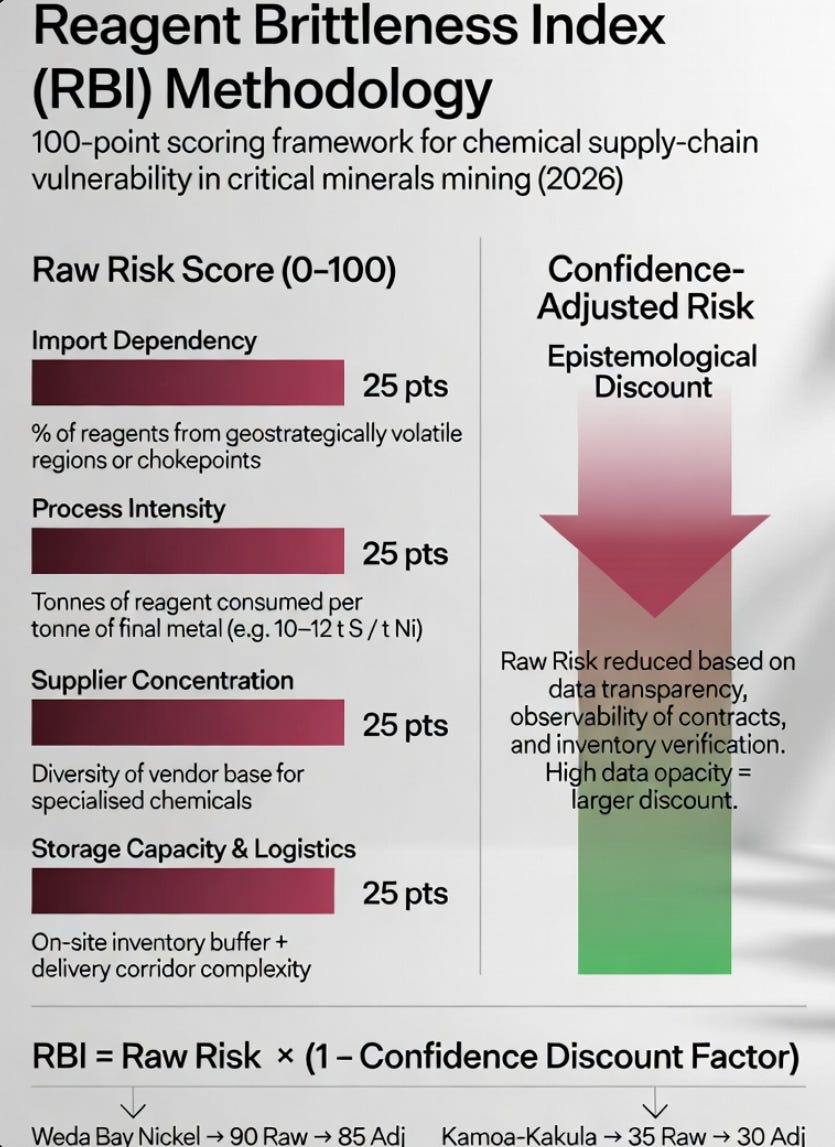

Methods Box: Measuring Reagent Brittleness

To quantify the supply chain vulnerabilities detailed in this report, we utilised our own metric, the Reagent Brittleness Index (RBI).

This framework evaluates the fragility of specific mining operations by analysing their dependence on critical chemical inputs, independent of underlying geological or reserve-based metrics.

The RBI relies heavily on observable supply chain data and operational parameters to construct a risk profile. It’s a risk-scoring system for evaluating miners’ reagent risks.

Import Dependency: Measures the percentage of required reagents (e.g., elemental sulphur, concentrated acid, specific solvent extractants) sourced from geostrategically volatile regions, penalising over-reliance on single transit chokepoints.

Process Intensity: Calculates the absolute volume of reagent consumed per tonne of refined metal produced (e.g., tonnes of H2SO4 per tonne of Cu cathode or Ni MHP). Higher intensity exponentially increases exposure to price shocks.

Supplier Concentration: Evaluates the diversity of the vendor base for highly specialised, difficult-to-substitute chemicals, such as organophosphorus extractants used in rare earth separation.

Storage Capacity & Logistics: Assesses the on-site inventory buffer (measured in operational days) and the complexity of the delivery corridor, acknowledging that corrosive and toxic reagents cannot be rapidly stockpiled or rerouted.

There are other considerations that could be added but these are the majors

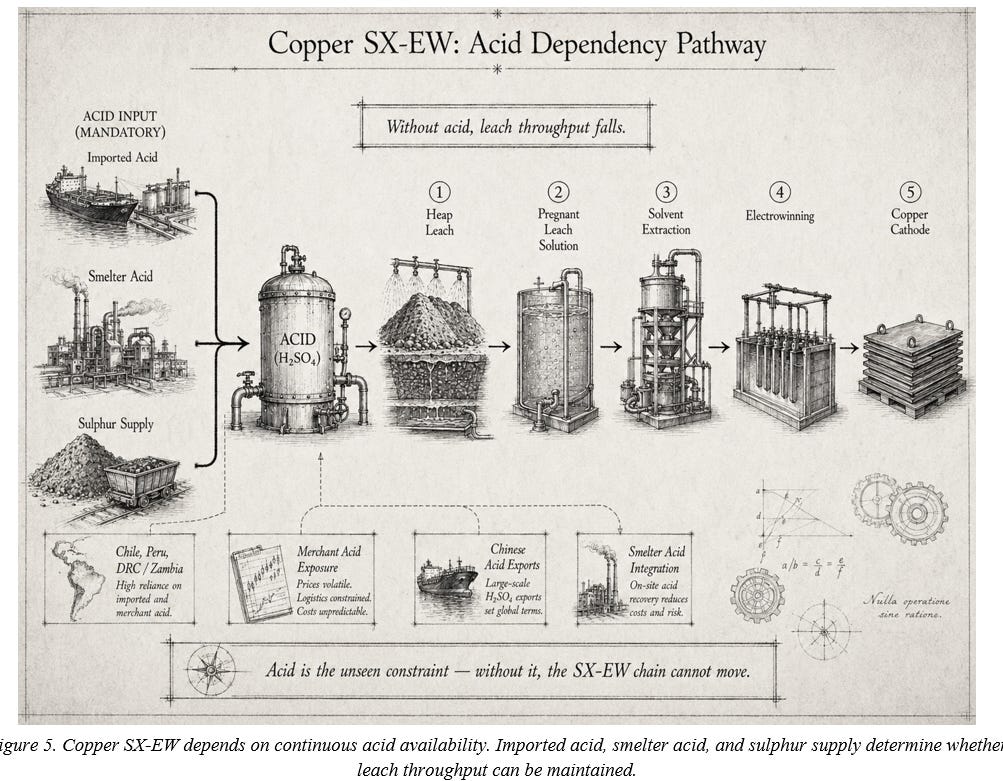

5. Copper SX-EW: The Acid Test in Chile and Africa

The solvent extraction and electrowinning (SX-EW) process is responsible for roughly one-fifth of the world’s primary refined copper production, representing an estimated 4 to 5 million tonnes annually technology operates by irrigating crushed oxide ores on lined heap leach pads with a weak sulphuric acid solution.

This pregnant leach solution (PLS) is gathered, concentrated using organic solvent extractants (often phenolic oximes), and subjected to an electrical current to deposit 99.99% pure copper cathodes

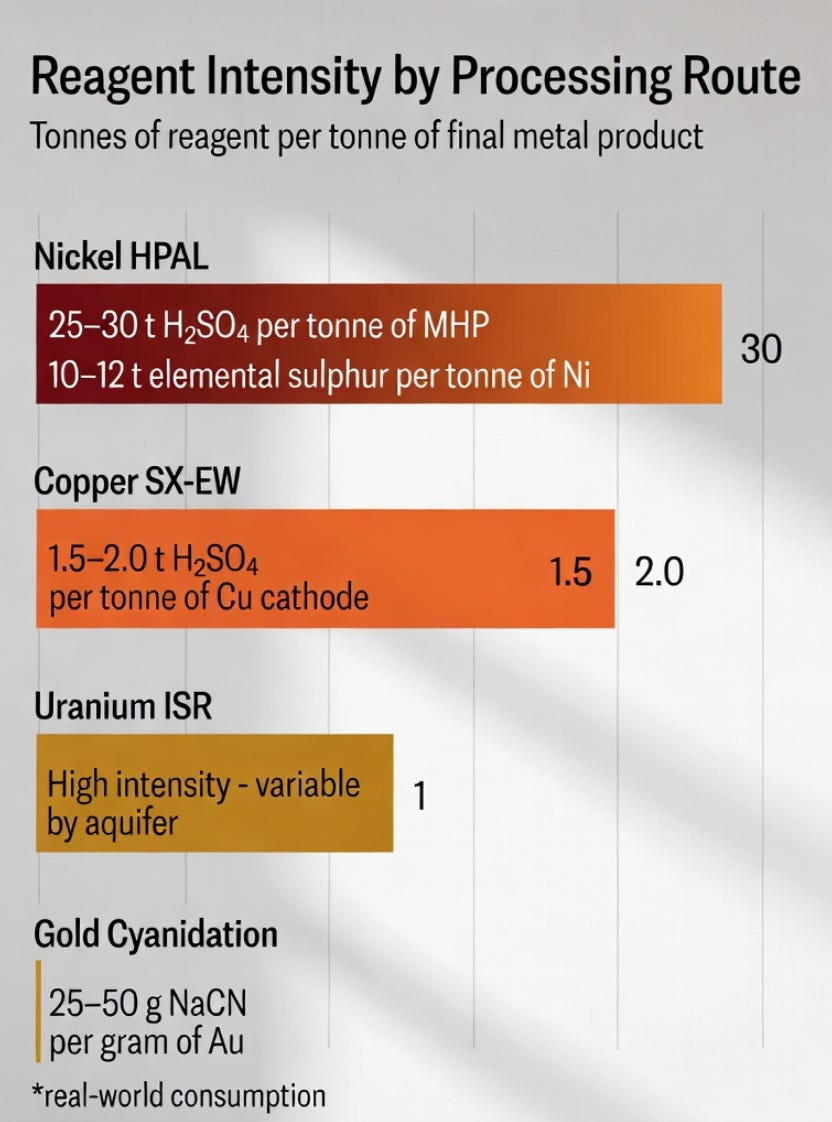

The chemical demands of this process are immense. Depending on the mineralogy and acid-consuming gangue materials present in the ore, SX-EW operations require between 1.5 and 2.0 tonnes of sulphuric acid per tonne of copper cathode produced

For regions heavily reliant on this processing route, the disruption to global acid flows is devastating.

Top exposed copper regions:

Chile: As the world’s largest copper producer, Chile generates over 1.1 million tonnes of its copper output

To sustain this, the country imports more than 1 million tonnes of sulphuric acid annually, with China serving as the primary supplier (accounting for roughly 37% of imports)

Chinese shipments to Chile plummeted from 151,268 tonnes in March 2025 to 31,870 tonnes in February 2026, and to absolute zero

Consequently, spot prices for delivered acid in Mejillones skyrocketed by 44% in a single month, doubling since February

Without access to Chinese merchant acid, operators are forced to throttle leach pad irrigation, directly threatening a significant contraction in national cathode output.

DRC: The central African copperbelt is heavily skewed toward hydrometallurgy, with SX-EW accounting for roughly half of the DRC’s copper output

The region imports approximately 2 million tonnes of elemental sulphur annually to feed captive acid-burning plants

Delivered trucking costs from the port of Dar es Salaam to Kolwezi run high; with maritime disruptions, landed sulphur prices approached $900 per tonne, resulting in synthetic acid costs nearing $300 per tonne, while merchant delivered acid prices reached $1,000–$1,400 per tonne

Zambia: Closely linked to the DRC’s processing ecosystem, Zambia suffers from the same logistical premiums and sulphur blockades.

In response to localised shortages, the Zambian government instituted a strict, permit-based export control system for sulphuric acid, further balkanising regional supply and preventing the free flow of reagents across the copperbelt.

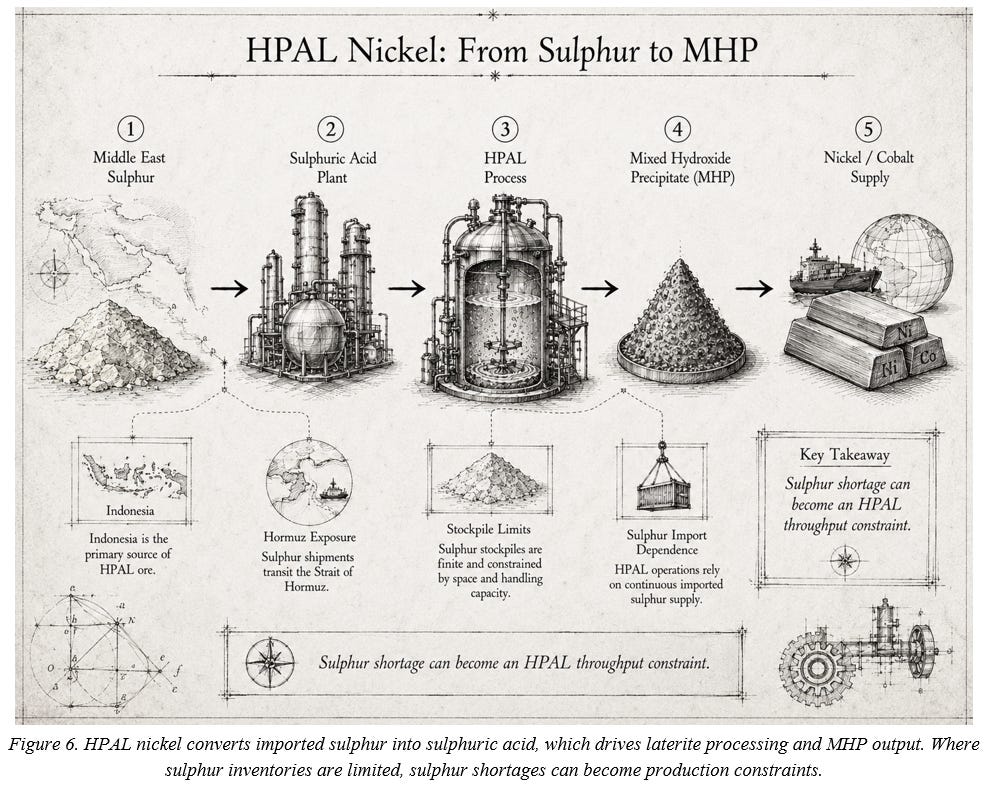

6. Nickel HPAL: The Indonesian Sulphur Dependency

The global nickel market’s expansion, driven predominantly by the electric vehicle battery sector, rests almost entirely on the proliferation of High-Pressure Acid Leaching (HPAL) facilities in Indonesia. HPAL technology utilises aggressive conditions, high temperatures (up to 250°C) and extreme pressures to dissolve nickel and cobalt from low-grade lateritic ores, ultimately precipitating a mixed hydroxide precipitate

The reagent intensity of HPAL is staggering. The process requires between 25 and 30 tons of sulphuric acid per ton of MHP produced, translating to approximately 10 to 12 tonnes of elemental sulphur required per tonne of contained nickel

Because Indonesian ores often possess high magnesium content, which is highly acid-consuming, the chemical efficiency of these operations is inherently brittle and highly wasteful, generating 1.2 to 1.6 tonnes of wet tailings per tonne of nickel.

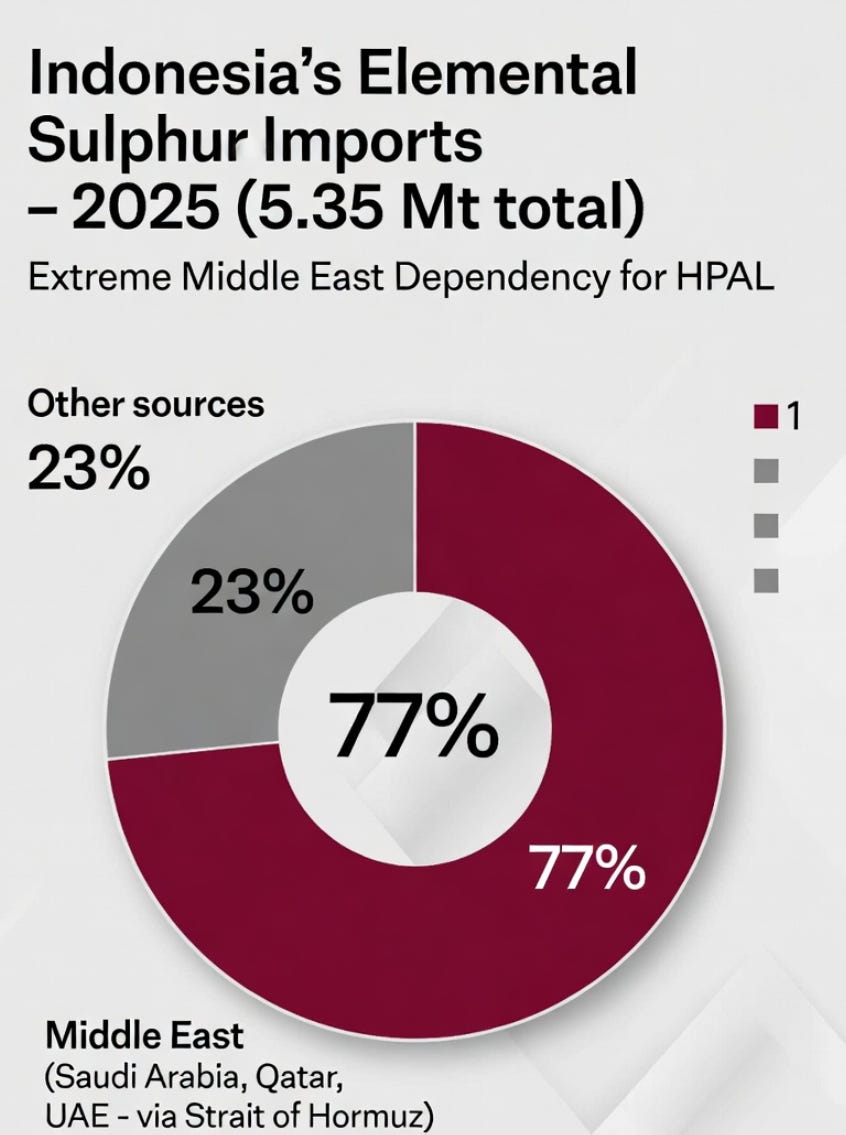

Indonesia produces over 50% of the world’s nickel but possesses minimal domestic sulphur resources. To feed the captive acid plants attached to its HPAL complexes, the country imported 5.35 million tonnes of elemental sulphur in 2025

Crucially, between 75% and 80% of this import volume originates in the Middle East, specifically Saudi Arabia (1.76 million tonnes), Qatar (930,500 tonnes), and the UAE

The disruption in the Strait of Hormuz has exposed the extreme fragility of this localised boom. Major Indonesian MHP producers, operating with minimal sulphur inventory buffers of only one to two months, were forced into immediate operational distress

Delivered sulphur prices in Indonesia spiked past $800 per tonne, with traders reporting spot deals reaching $1,000 per tonne, Reuters, “Indonesia nickel makers trim battery-feed output,” April 14, 2026.

The surge in feedstock costs added an estimated $4,000 per tonne to the cost of Indonesian HPAL nickel production, severely compressing margins and pushing LME nickel prices to 11-week highs

In response, major operators, including Huafei Nickel Cobalt (a subsidiary of Huayou), were forced to place up to half of their MHP capacity on temporary care and maintenance, citing unsustainable input costs

7. Uranium ISR: Kazatomprom’s Acid Deficit

The uranium sector represents another critical node paralysed by the reagent squeeze. In 2022, over 56% of global uranium was mined via in-situ recovery

In situ leach mining of uranium. This technique involves injecting chemical leaching solutions directly into underground, porous sandstone aquifers to dissolve the uranium, then pumping the pregnant solution to the surface for extraction, resulting in virtually zero surface tailings.

Kazakhstan, which dominates global supply with nearly 40% of the world’s uranium output, relies exclusively on ISR, Kazatomprom.

Unlike ISR operations in the United States that utilise alkaline leaching due to carbonate-heavy geology, or Australian operations that utilise hydrogen peroxide oxidants, Kazakh ISR relies on highly concentrated injections of pure sulphuric acid into the orebody.

The national operator, Kazatomprom, consumed approximately 1.85 million tonnes of sulphuric acid in 2025

As domestic agricultural demand for phosphate fertilisers competes for limited national acid supply, and regional imports become constrained by the broader global sulphur deficit and Russian export bans, Kazatomprom’s ambitious expansion plans have faltered. The company was forced to aggressively downgrade its 2025 production guidance from an anticipated 30,500–31,500 tonnes of uranium (tU) down to a revised 25,000–26,500 tU (on a 100% basis)

This shortfall of roughly 5,000 tU, or approximately 13 million pounds of U3O8, represents a massive contraction equivalent to nearly 5% of primary global supply

Operations such as the Budenovskoye joint venture have seen output targets drastically curtailed, dropping from 4,000 tonnes to 1,300 tonnes in 2025 and from 6,000 tonnes to 3,750 tonnes in 2026. Kazatomprom, “Financial Results,” 2025.

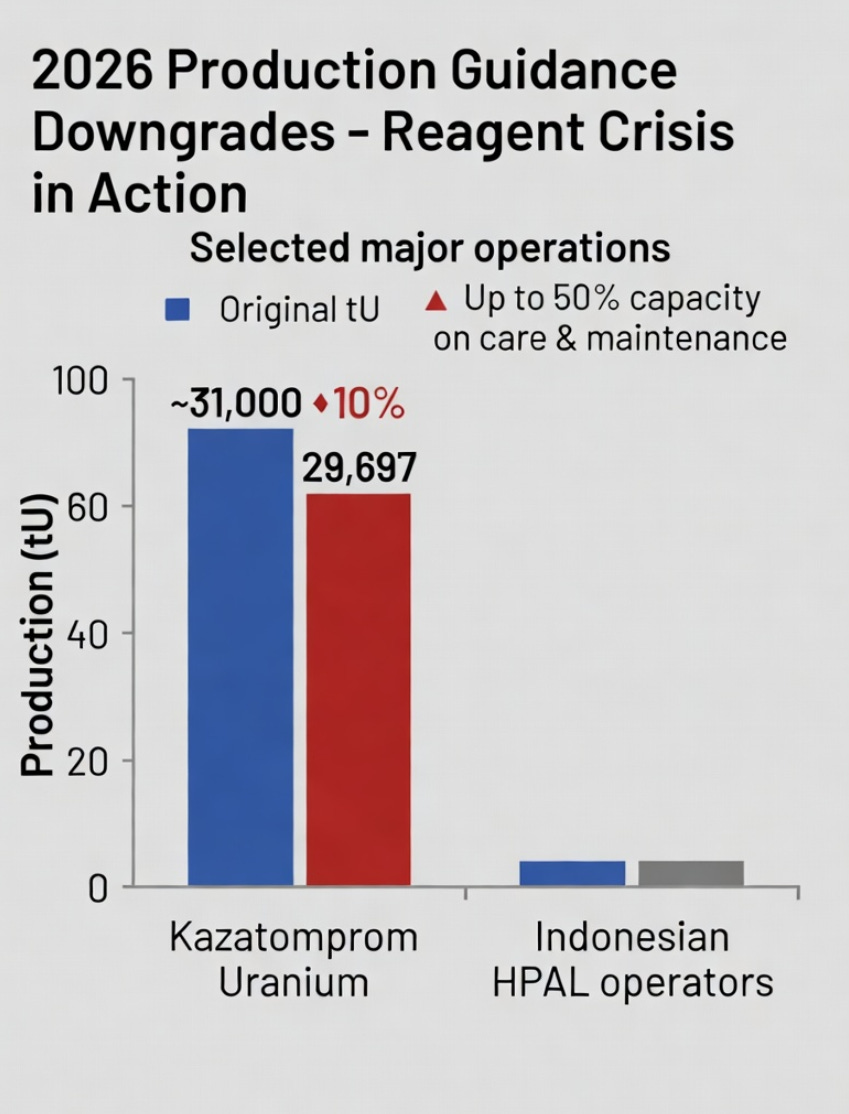

Furthermore, Kazatomprom announced that its 2026 production target would be cut by 10%, reducing nominal output from 32,777 tU to 29,697 tU

To mitigate this crippling dependency, Kazatomprom is accelerating the construction of a dedicated 800,000-tonne-per-year domestic sulphuric acid plant (Taiqonyr Qyshqyl Zauyty LLP) in the Turkestan region, though this strategic buffer will not reach full operational capacity until late 2026. Kazatomprom,

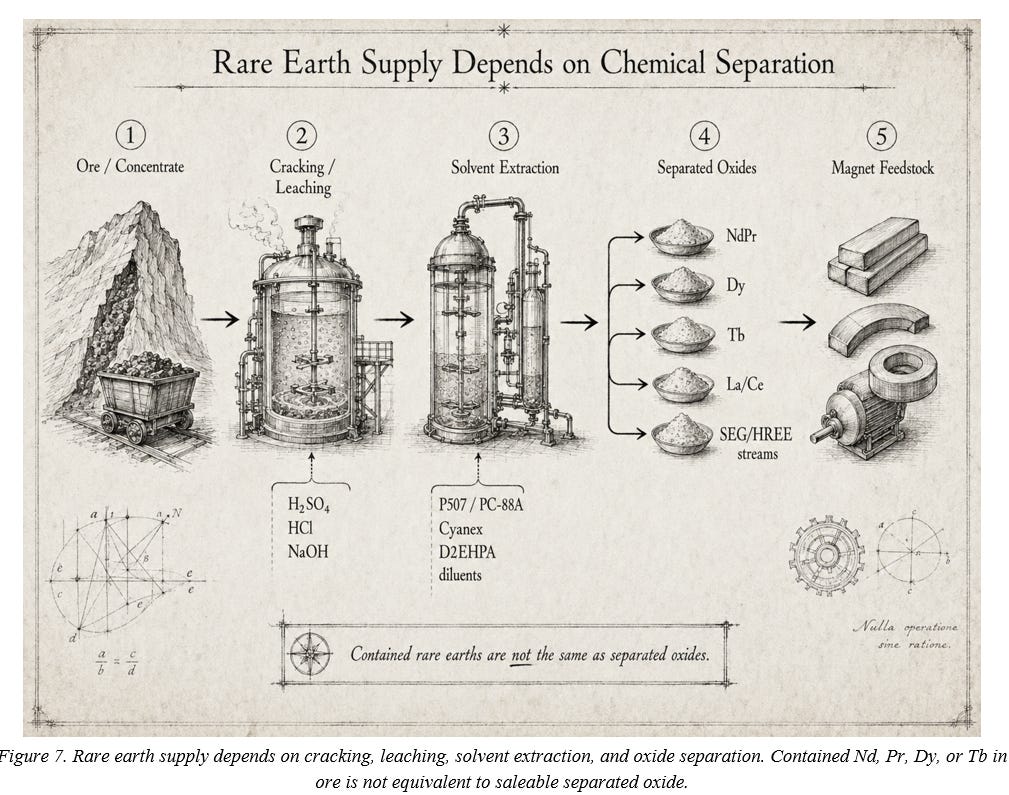

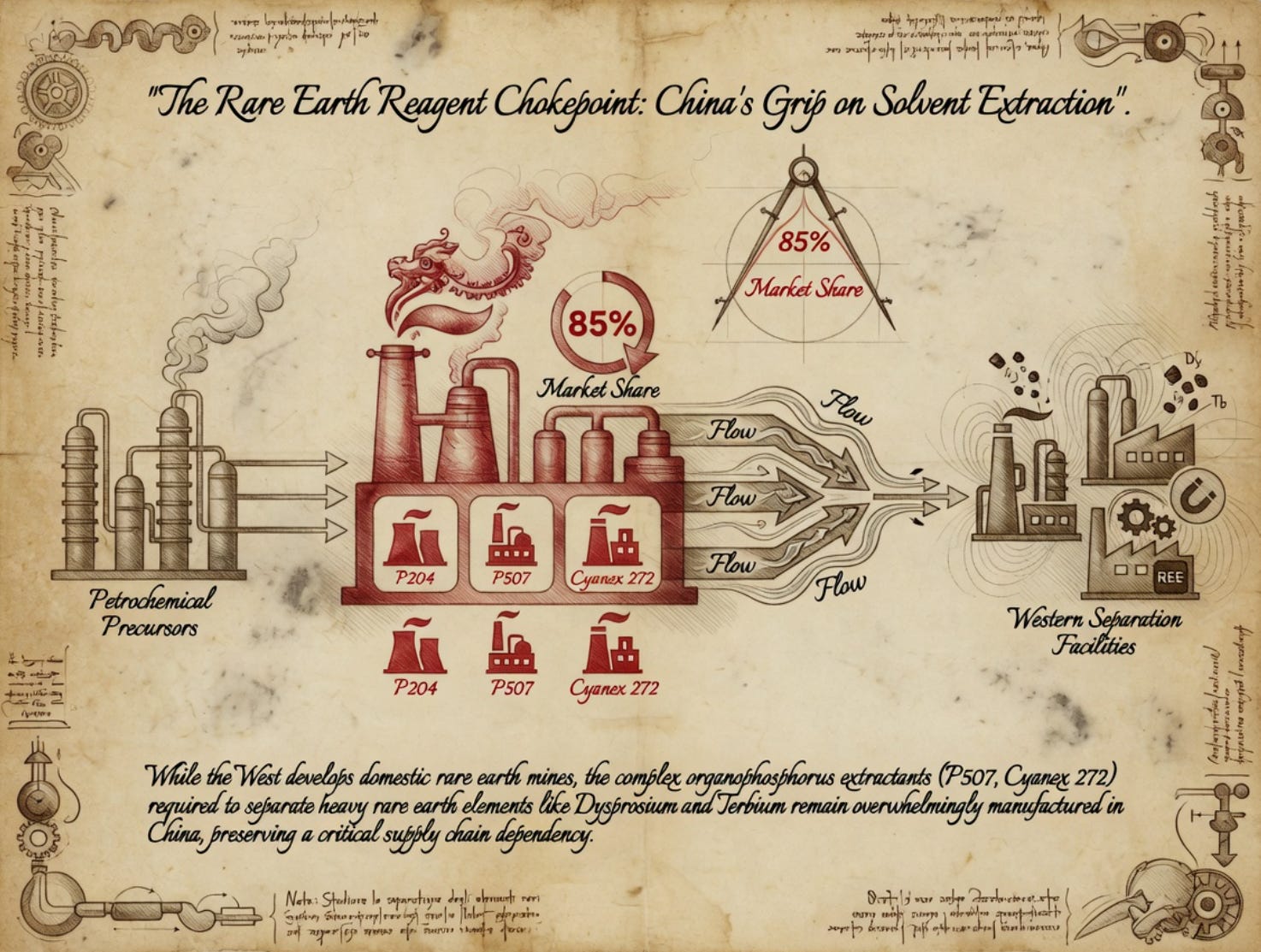

8. Rare Earth Elements: The Specialised Extractant Chokepoint

While base metals and uranium are constrained by the bulk tonnage of sulphuric acid, the rare earth element (REE) sector is bottlenecked by highly specialised, low-volume organic chemistry.

The 17 rare earth elements possess nearly identical physical and chemical properties, with ionic radii ranging from 0.88 to 1.02

Separating them from a mixed mineral concentrate into high-purity individual oxides requires vast arrays of solvent extraction mixer-settler units, often numbering in the hundreds or thousands of stages

This separation process is entirely dependent on specific organophosphorus extractants that selectively chelate target metal ions. For light rare earths, Di-(2-ethylhexyl) phosphoric acid (D2EHPA or P204) is the industry standard

For the highly valuable heavy rare earths, such as dysprosium and terbium, critical for permanent magnets in wind turbines and EV motors, advanced reagents like 2-ethylhexylphosphonic acid mono-2-ethylhexyl ester (P507 / PC-88A) and bis(2,4,4-trimethylpentyl)phosphinic acid (Cyanex 272) are mandatory to achieve commercial-grade purity levels above 99.5% MDPI

These extractants rely on petrochemical precursors and sophisticated chemical synthesis. Currently, China controls an estimated 85% of the global manufacturing capacity for these specialised chemicals, alongside dominance in crucial precipitants like oxalic acid (exporting nearly 298 million kg globally in 2023) and ammonium chloride

The Western ambition to build an independent “mine-to-magnet” supply chain is fundamentally hollow without a secure, non-Chinese source for these extraction reagents.

If a newly commissioned Western refinery relies entirely on Chinese-manufactured P507 to separate its heavy rare earths, the geopolitical dependency has merely shifted downstream from the ore to the chemical input

Furthermore, operations outside China, such as Lynas Rare Earths’ Kalgoorlie cracking and leaching plant in Western Australia, face compounding infrastructure risks; recent severe power grid disruptions in November 2025 caused significant shortfalls in mixed rare earth carbonate (MREC) output, underscoring the fragility of complex, reagent-dependent continuous processing facilities operating outside established industrial clusters

9. Gold Cyanidation: The Ammonia-Gas Link

Gold mining relies on chemical processing as heavily as base metals, predominantly utilising sodium cyanide (NaCN) in vat leaching, heap leaching, and carbon-in-pulp (CIP) circuits. Sodium cyanide forms highly stable, water-soluble aurocyanide complexes, allowing for extraction efficiencies frequently exceeding 90% even from microscopic gold particles dispersed in complex gangue

While theoretical cyanide consumption can be as low as 0.5 grams per gram of gold, real-world operations typically consume 25 to 50 grams of cyanide per gram of gold due to the presence of reactive copper minerals and iron sulphides that consume the reagent.

Globally, the gold mining sector consumes in excess of 1 million tonnes of sodium cyanide annually, accounting for roughly 85% of total NaCN demand

The supply chain for sodium cyanide is intrinsically tied to global petrochemical and energy markets.

The dominant commercial production route, the Andrussow process, synthesises high-purity hydrogen cyanide from ammonia, natural gas (methane), and air over a platinum-rhodium catalyst at extreme temperatures (approx. 1050°C).

The hydrogen cyanide is subsequently neutralised with sodium hydroxide to yield solid sodium cyanide briquettes or liquid solutions,

To manufacture one tonne of sodium cyanide, the process requires approximately 4,350 Nm3 of air, 0.59 tons of ammonia, 6.66 tons of natural gas, 0.30 tons of sulfuric acid, and 0.90 tons of sodium hydroxide

Consequently, the cost and availability of NaCN are highly sensitive to price fluctuations in natural gas and ammonia feedstocks.

The vulnerability of this supply chain was demonstrated in November 2025, when Sasol, the sole domestic producer of liquid cyanide in South Africa, declared force majeure following a catastrophic breakdown at its ammonia plant, significantly disrupting the country’s gold mining industry and forcing reliance on solid cyanide stockpiles

Beyond feedstock dependencies, sodium cyanide is an acutely toxic, GHS Category 1 hazardous material, demanding stringent, specialised logistics governed by the International Cyanide Management Code (ICMC)

To insulate themselves from deep-sea logistics disruptions and freight cost volatility, the industry is seeing a structural shift toward localised production hubs.

For example, Draslovka’s expansion to supply Nevada Gold Mines natively, or the development of a 50,000-tonne modular sodium cyanide plant in Egypt, leverages existing domestic natural gas and ammonia networks to secure reagent supply directly for regional mining operations, bypassing maritime chokepoints entirely

10. Alumina Refining: Caustic Soda Dynamics

The processing of bauxite ore into alumina (aluminium oxide) via the Bayer process highlights yet another critical reagent dependency: caustic soda (sodium hydroxide, NaOH).

In the initial digestion phase of the Bayer process, finely ground bauxite is subjected to elevated temperatures (150°C to 270°C) and pressures in a highly concentrated caustic soda solution.

The strong alkali selectively dissolves the alumina content to form sodium aluminate, while leaving insoluble iron oxides and silica to be filtered out as waste “red mud”

The Bayer process is exceptionally reagent-intensive. The global average consumption is approximately 100 kilograms of caustic soda per tonne of alumina produced, though this varies significantly based on the reactive silica content of the specific bauxite ore, which consumes caustic soda to form unwanted sodium-aluminium-silicate desilication products (DSP)

Because alumina production occurs at a massive scale, surpassing 147 million tonnes globally in 2024, the aluminium industry stands as the single largest end-user of caustic soda, accounting for over 20% of global demand (representing 57.0% of the market share for liquid lye) .

The vulnerability of the caustic soda supply chain is rooted in its manufacturing method.

Sodium hydroxide is produced alongside chlorine via the electrolysis of brine in the chlor-alkali process. This electrochemical conversion is immensely energy-intensive; modern membrane cell technologies consume between 2,200 and 2,700 kWh per metric ton of caustic soda

Consequently, caustic soda production costs are inextricably linked to regional electricity prices. When global energy markets experience extreme volatility—such as the 40% to 60% spikes in European and Asian natural gas futures triggered by Middle Eastern instability and LNG suspensions—the cash costs of operating chlor-alkali plants surge dramatically

This energy-driven margin compression forces producers to raise prices or curtail output, directly inflating the operating expenses of downstream alumina refineries and exposing the broader aluminium market to cascading power-cost shocks.

11. Reagent Brittleness Index (RBI) & Confidence-Adjusted Risk

The cascading impacts of the 2026 supply shocks underscore the absolute necessity of moving beyond traditional resource evaluations to systematically assess chemical supply chain risks. The Reagent Brittleness Index (RBI) provides a 100-point scoring framework to quantify these vulnerabilities.

Within the RBI framework, a critical distinction must be drawn between Raw Risk and Confidence-Adjusted Risk.

Raw Risk represents the theoretical, inherent vulnerability of a specific asset based purely on its flowsheet and geographic location. It scores an operation based on absolute physical dependencies:

What is the exact tonnage of sulphuric acid required per tonne of cathode?

What percentage of elemental sulphur must transit a contested maritime chokepoint to reach the facility?

How concentrated is the supplier base for a highly specific solvent extractant?

A high Raw Risk score indicates an asset whose operational continuity is highly leveraged to fragile, external chemical supply lines.

Confidence-Adjusted Risk, however, incorporates an epistemological discount based on the quality, transparency, and observability of the underlying supply chain data.

In opaque markets, such as the spot procurement of reagents in Central Africa or the sourcing agreements for proprietary rare-earth extractants, analysts frequently lack verifiable, real-time data on on-site inventory buffers, exact contractual pricing structures, or specific supplier identities.

When the evidentiary baseline relies on industry averages, estimated storage capacities, or generalised trade flow assumptions rather than audited corporate disclosures, the RBI applies a “Confidence Discount.”

This discount penalises the Raw Score to reflect the margin of error inherent in poor data environments. Therefore, an asset may have a high Raw Risk due to its known reliance on imported acid, but its Confidence-Adjusted Risk score will be lower, reflecting that unobservable mitigations (such as undisclosed localised stockpiling or unannounced supply diversification) may exist, making the worst-case assessment less definitive.

The important point is not that every variable is perfectly observable. Rather, the architecture of the measurement framework allows analysts to isolate where data opacity specifically inflates risk. As supply chain transparency improves, the gap between Raw Risk and Confidence-Adjusted Risk will narrow, providing a clearer baseline for asset valuation.

12. What to Watch Next

As the mining sector grapples with the permanent reality of constrained chemical inputs, the industry is forced to adapt its strategic positioning.

The era of assuming frictionless, infinite access to cheap industrial reagents is definitively over. So must be the valuations that are aligned to those obsolete conditions

Analysts and operators must closely monitor several evolving dynamics that will dictate the future viability of marginal mineral assets.

First, vertical integration will become a premium differentiator. Mining operations that invest heavily in captive acid-generating facilities, elemental sulphur recovery units, or on-site chlor-alkali cells will insulate themselves from merchant market volatility.

Joint ventures, such as Fitzroy Minerals utilising third-party SX-EW infrastructure to bypass the capital intensity of establishing new, acid-constrained processing circuits, will likely become more prevalent

Companies with internal reagent security, such as Ivanhoe Mines, which generates massive byproduct acid, will command higher valuation multiples than those exposed to spot-market procurement.

Second, the geopolitical weaponisation of reagents will intensify. As demonstrated by China’s sulphuric acid export ban, nations possessing massive downstream refining capacity will increasingly leverage bulk chemicals to protect domestic industries and exert pressure on international supply chains. Mining jurisdictions must secure bilateral trade agreements for chemical inputs alongside the physical off-take of the refined metals.

Finally, necessity will accelerate technological substitution. To reduce reliance on massive volumes of sulphuric acid and hazardous sodium cyanide, the industry will allocate significant R&D capital to alternative hydrometallurgical pathways. Innovations in direct lithium extraction (DLE), advanced bio-leaching utilising engineered microbial cultures, and the commercialisation of benign, biodegradable frothers and collectors to replace petrochemical-derived xanthates will advance

Operations that successfully implement flowsheet modifications to reduce overall chemical intensity per tonne of metal recovered will possess the ultimate competitive advantage in a chemically constrained future.

The illusion has finally cracked.

For decades, the mining industry fixated on geological reserves while treating sulphuric acid, sodium cyanide and organophosphorus extractants as mere background consumables.

In the first half of 2026, the Strait of Hormuz and China’s acid export ban ripped away the veil: modern metallurgy is chemically hostage. The true bottleneck in the energy transition is no longer how much metal sits in the ground; it is who can reliably secure the reagents required to liberate it.

Geological scarcity has been overtaken by chemical and geopolitical vulnerability. From this point forward, the most valuable mining assets will not be those with the largest deposits, but those with the most resilient, vertically integrated, or geographically secure chemical supply chains.

The invisible choke is now brutally visible, and it will redraw the cost curves, valuations, and strategic map of the entire critical minerals industry.

Sulphur & Acid Supply Risk Dashboard: Critical Mining Assets

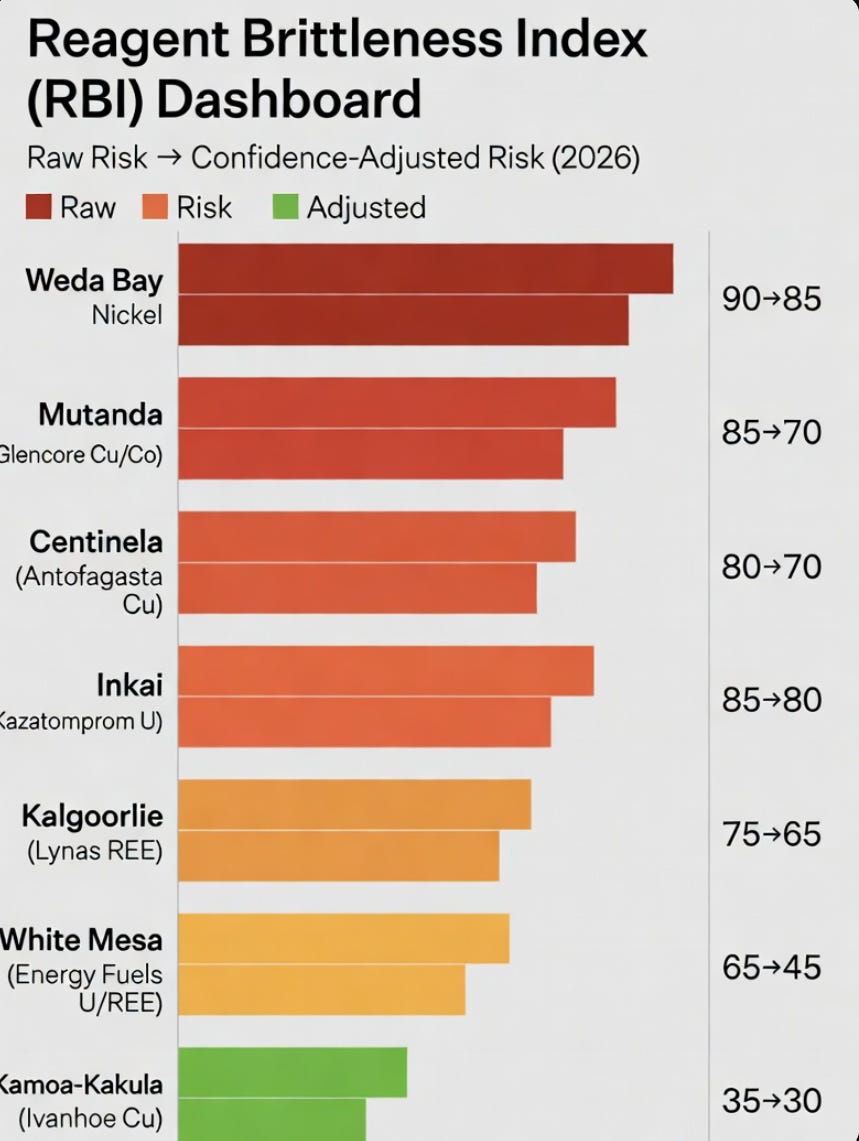

Mine=Mutanda

Glencore $GLNCY Copper/Cobalt

Raw: 85 → Adj Score: 70

Sulphur supply dependent on African logistical corridors; highly exposed to Middle Eastern sulphur shocks.

Mine=Centinela

Antofagasta $ANTO • Copper

Raw: 80 → Adj Score: 70

Sulphuric acid storage buffer is estimated to be heavily reliant on seaborne acid imports into Chile.

Mine=Weda Bay

Tsingshan/Eramet $ERA.PA • Nickel

Raw: 90 → Adj Score: 85

HPAL operations require 10-12 tonnes of sulphur per tonne of MHP; absolute reliance on imported Middle Eastern sulphur.

Mine=White Mesa

Energy Fuels (UUUU 0.00%↑ ) • Uranium/REE

Raw: 65 → Adj Score: 45

REE extractant supply is heavily constrained globally (Supplier diversified - Low Confidence).

Mine=Kamoa-Kakula

Ivanhoe Mines ($IVN) • Copper

Raw: 35 → Adj Score: 30

Low risk due to internal 1,350 tpd high-strength sulphuric acid byproduct generation.

Mine=Kalgoorlie

Lynas Rare Earths ($LYC.AX) • REE

Raw: 75 → Adj Score: 65

High vulnerability to local power grid infrastructure failures, disrupting continuous chemical processing.

Mine=Inkai

Kazatomprom ($KAP) • Uranium

Raw: 85 → Adj Score: 80

Acute domestic sulphuric acid deficit restricting ISR production targets; dedicated acid plant not online until late 2026.

Hydrometallurgy Reagent Risk Comparison

• Primary Reagent: Sulphuric Acid (H₂SO₄)

• Process Intensity: 1.5 – 2.0 tonnes H₂SO₄ per tonne of Cu Cathode

• Global Import Reliance: Chile imports >1,000,000 tonnes annually, heavily dependent on China (37% of imports)

• Recent Cost Impact: Spot prices for delivered acid in Mejillones skyrocketed +44% in one month

• Primary Reagent: Elemental Sulphur (for H₂SO₄)

• Process Intensity: 10 – 12 tonnes of Sulphur per tonne of Ni in MHP

• Global Import Reliance: 75% to 80% of Indonesian sulphur imported directly from the Middle East via the Strait of Hormuz

• Recent Cost Impact: Spot sulphur prices delivered rose from $500 to >$800–$1,000/tonne, adding $4,000/t to Ni cost

• Primary Reagent: Sulphuric Acid (H₂SO₄)

• Process Intensity: Highly variable based on aquifer geology

• Global Import Reliance: High domestic reliance; consumed 1.85 million tonnes in 2025

• Recent Cost Impact: 2026 production guidance downgraded by 10% (32,777 tU to 29,697 tU) due to acid deficits

Gold Cyanidation (Emerging Shortage)

• Primary Reagent: Sodium Cyanide (NaCN)

• Process Intensity: 25 – 50 grams NaCN per gram of Gold

• Global Import Reliance: Moderate. Localised production hubs (e.g., US, Egypt) bypass maritime transit

• Recent Cost Impact: High sensitivity to natural gas and ammonia feedstock prices for HCN precursors

Chart Deck

Chart 1: Global Sulphuric Acid Demand Split

The Metals-vs-Food Paradox in one chart: 57% of the world’s sulphuric acid goes to fertiliser. Every extra tonne of battery nickel or copper cathode is acid that could have grown food.

Chart 2: Sulphur Trade Collapse

Seaborne sulphur loadings collapsed 31.2% in one month after Hormuz. Persian Gulf exports fell 65.9%. This is the upstream shock that starved acid plants worldwide.

Chart 3: China Acid Export Ban Impact

China’s May 1, 2026, acid export ban removed the global balancing supply. The downstream multiplier that turned the sulphur shock into a full crisis.

Chart 4: Reagent Intensity Comparison

HPAL nickel is 10–12× more sulphur-intensive than copper SX-EW. This is why Indonesia felt the shock first and hardest.

Chart 5: RBI Dashboard

The RBI in action. Weda Bay, Mutanda and Centinela are flashing red. Kamoa-Kakula is the only green. Vertical integration wins every time, and Ivanhoe is a vertically integrated mine

Chart 6: Indonesian Sulphur Dependency

75–80% of Indonesia’s sulphur for nickel HPAL came straight through Hormuz. When the strait closed, delivered prices hit $800–$1,000/t overnight.

Chart 7: Production Guidance Downgrades

From guidance to reality: acid shortages forced Kazatomprom to cut ~5,000 tU and Indonesian HPAL producers to idle up to 50% of capacity. This is the new cost-curve reality. Note, Kazatomprom are urgently building acid production online status is hard to ascertain, but maybe by early 2027

Introducing the Reagent Brittleness Index (RBI) , the new 100-point framework that actually predicts which miners survive the 2026 acid & reagent crisis. Raw Risk vs Confidence-Adjusted Risk explained in one visual. Vertical integration = green. Spot-market dependency = red

{

"metadata": {

"title": "The Invisible Constriction",

"author": "Craig Tindale",

"publish_date": "2026-05-16",

"version": "1.0",

"description": "The 2026 reagent crisis: from geological scarcity to chemical supply-chain choke point in critical minerals"

},

"core_thesis": "The mining industry has shifted from geological scarcity to chemical-input bottlenecks. Modern metallurgy is now hostage to specialised reagents (especially sulphuric acid) whose supply chains are geopolitically weaponisable. This creates a zero-sum metals-versus-food paradox that decarbonisation has unintentionally deepened.",

"key_shocks": {

"hormuz_closure": {

"date": "late February 2026",

"impact": "Severed primary artery for ~50% of world seaborne elemental sulphur trade. Global sulphur loadings collapsed 31.2% MoM (March 2026); Persian Gulf exports fell 65.9%.",

"price_spikes": {

"Mediterranean": "$155/t → >$400/t",

"Indonesia": "~$500/t → $800–$1,000/t"

}

},

"china_acid_ban": {

"date": "May 1 2026",

"impact": "Removed ~3 Mt annualised seaborne sulphuric acid supply. China produced ~120 Mt acid in 2025 and was the global swing exporter.",

"q1_2026_reduction": "700 kt exported vs 1.3 Mt in 2025"

}

},

"metals_vs_food_paradox": {

"sulphuric_acid_demand_split": "55–60% fertiliser industry; mining = fraction of total",

"competition": "Molecule-for-molecule: every extra tonne of copper cathode, nickel MHP or uranium yellowcake consumes acid that could have produced phosphate fertiliser"

},

"reagent_brittleness_index": {

"methodology": "100-point score based on Import Dependency + Process Intensity + Supplier Concentration + Storage & Logistics. Raw Risk (theoretical) vs Confidence-Adjusted Risk (epistemological discount for data opacity).",

"dashboard": [

{

"mine": "Mutanda",

"company": "Glencore $GLNCY",

"commodity": "Copper/Cobalt",

"raw_risk": 85,

"adj_risk": 70,

"primary_vulnerability": "Sulphur supply via African corridors + Middle East shocks"

},

{

"mine": "Centinela",

"company": "Antofagasta $ANTO",

"commodity": "Copper",

"raw_risk": 80,

"adj_risk": 70,

"primary_vulnerability": "Seaborne acid imports into Chile"

},

{

"mine": "Weda Bay",

"company": "Tsingshan/Eramet $ERA.PA",

"commodity": "Nickel",

"raw_risk": 90,

"adj_risk": 85,

"primary_vulnerability": "HPAL — 10–12 t sulphur per t Ni MHP + 75–80% Middle East sourcing"

},

{

"mine": "White Mesa",

"company": "Energy Fuels",

"commodity": "Uranium/REE",

"raw_risk": 65,

"adj_risk": 45,

"primary_vulnerability": "REE extractant supply (diversified but low confidence)"

},

{

"mine": "Kamoa-Kakula",

"company": "Ivanhoe Mines $IVN",

"commodity": "Copper",

"raw_risk": 35,

"adj_risk": 30,

"primary_vulnerability": "None — on-site smelter produces 1,350 tpd acid"

},

{

"mine": "Kalgoorlie",

"company": "Lynas Rare Earths $LYC.AX",

"commodity": "REE",

"raw_risk": 75,

"adj_risk": 65,

"primary_vulnerability": "Organophosphorus extractants + power-grid risk"

},

{

"mine": "Inkai",

"company": "Kazatomprom $KAP",

"commodity": "Uranium",

"raw_risk": 85,

"adj_risk": 80,

"primary_vulnerability": "Domestic acid deficit; new plant not online until late 2026"

}

]

},

"process_intensities": {

"copper_sx_ew": "1.5–2.0 t H₂SO₄ per t Cu cathode",

"nickel_hpal": "25–30 t H₂SO₄ per t MHP (10–12 t elemental sulphur per t Ni)",

"uranium_isr_kazakhstan": "Highly variable; Kazatomprom consumed 1.85 Mt acid in 2025",

"gold_cyanidation": "25–50 g NaCN per g Au (real-world)",

"alumina_bayer": "100 kg NaOH per t alumina"

},

"commodity_exposures": {

"copper": "Chile imports >1 Mt acid/yr (37% from China pre-ban); DRC & Zambia exposed to trucking + sulphur premiums",

"nickel": "Indonesia imported 5.35 Mt sulphur in 2025 (75–80% Middle East); up to 50% HPAL capacity idled",

"uranium": "Kazatomprom downgraded 2025 output by ~5,000 tU and 2026 target by 10%",

"ree": "85% global capacity for P507 / Cyanex 272 etc. still in China",

"gold": "NaCN supply tied to ammonia + natural gas (Andrussow process)",

"alumina": "Caustic soda costs linked to chlor-alkali power prices"

},

"charts": [

{ "id": 1, "title": "Global Sulphuric Acid Demand Split", "data_note": "57% fertiliser → metals-vs-food paradox" },

{ "id": 2, "title": "Sulphur Trade Collapse", "data_note": "31.2% MoM drop post-Hormuz" },

{ "id": 3, "title": "China Acid Export Ban Impact", "data_note": "May 1 2026 ban removed ~3 Mt seaborne supply" },

{ "id": 4, "title": "Reagent Intensity Comparison", "data_note": "HPAL nickel 10–12× more sulphur-intensive than SX-EW copper" },

{ "id": 5, "title": "RBI Dashboard", "data_note": "Weda Bay/Mutanda red; Kamoa-Kakula green" },

{ "id": 6, "title": "Indonesian Sulphur Dependency", "data_note": "75–80% via Hormuz" },

{ "id": 7, "title": "Production Guidance Downgrades", "data_note": "Kazatomprom -10% 2026; Indonesian HPAL -50% capacity" }

],

"conclusions_and_watchpoints": [

"Vertical integration (captive acid plants) now commands valuation premium",

"Geopolitical weaponisation of reagents is permanent policy tool",

"Technological substitution (bio-leaching, DLE, alternative extractants) will accelerate",

"Most valuable assets = those with resilient chemical supply chains, not largest deposits",

"The invisible choke is now brutally visible — cost curves, valuations and strategy are being redrawn"

]

}

I am starting to think humanity has a couple of options: a) quit geopolitical FAFO and get down to the economics of continuing humanity's advance or 2) just drop the pretense and get down to fighting a Third World War which will probably kill most of the extant human race and leave the few survivors at a prehistoric level of existence...

Which image generator do you use your amazing graphics? Your pictures paint far more than a thousand words…