We Need to Build The Pilbara Processing Commons

How Western Australia Can Capture the Critical Minerals Value Now Lost Offshore

Karratha, Western Australia | June 24–25 2026

Executive Summary

The West is unintentionally transferring $20–28 billion annually in critical minerals value to China, a loss projected to grow to $150–220 billion over the next decade. This transfer occurs via the export of unprocessed mineral concentrates, thereby losing downstream processing opportunities.

By shipping raw ore to Chinese refiners, Western producers enable them to capture high-value by-product metals such as gallium, scandium, and other rare earth elements. These metals are rarely (if ever) mined as primary products anywhere on Earth; they are recovered exclusively as derivatives during the processing of other ore bodies.

A detailed analysis of this dynamic is available in the companion essay, The Hidden Subsidy: Who Owns the Chemistry That Turns Metal Into Power.

This situation leaves substantial untapped value on the table, value that WA and processors are well-positioned to capture, delivering strong returns on investment.

Capital is shifting away from simple geology-focused projects toward the development of integrated processing hubs, with investors favouring jurisdictions that offer pre-built shared infrastructure. This report compares three leading models and provides a practical, actionable blueprint to capitalise on the opportunity.

This paper builds on a simple fact: many critical minerals are not mined directly. Gallium, indium, germanium, tellurium, selenium, scandium, and other strategic metals are often recovered during the processing of bauxite, zinc, copper, mineral sands, and other host materials. When Western producers export these materials offshore for refining, the processor captures not only the headline metal but also the by-product value, refining margin, technical knowledge and strategic leverage. China has built an integrated processing architecture that captures these derivative metals at scale. The Pilbara opportunity is to reverse that flow by creating a shared processing commons in Western Australia.

The Evolving Mine-to-Metal Complex

Western exporters of copper concentrate, zinc concentrate, bauxite intermediates, and other critical mineral feedstocks are unintentionally subsidising Chinese refining operations at scale.

This report compares the leading processing models and shows why the Pilbara has the strongest long-term opportunity to capture value through shared infrastructure, mineral stacking and common-user processing.

Western mines are shipping various ores to China for refining, where derivative metals are extracted and sold back to the West at very high prices, without payment to the miner for any of that value.

Gallium provides a clear example. It is recovered as a by-product of refining bauxite into aluminium and currently represents an estimated US$500 million annual market, with some expectations of rapid future growth. China controls about 93% of the market, capturing this value without paying miners separately for gallium because it is embedded in the bauxite stream. The table below identifies other under-accounted metals that move through the same system.

Because Western Australia exports such large volumes of mineral feedstock, it bears a disproportionate share of the loss in value. That makes this one of the largest industrial opportunities available to the state.

China owns the current game. Camaçari proves the commons model works. The Pilbara has the richest ore streams and greenest energy; it simply needs to install the shared plumbing (like Cetrel + Boodarie commons) to leapfrog both and claim the highest added value and market share in the Western world.

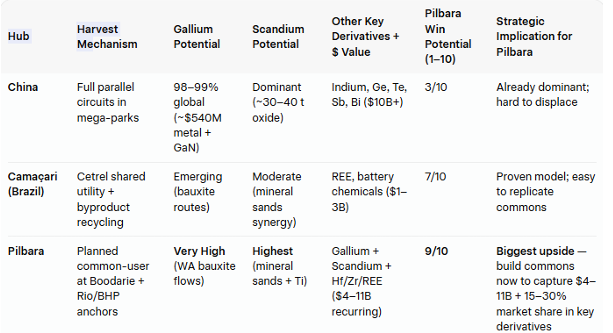

The Three Competing Processing Architectures — Size Comparison

To truly grasp what the Pilbara can become, picture three distinctly different “industrial kitchens” — advanced processing ecosystems that take raw mineral ores and concentrates and transform them into a rich menu of high-value metals, chemicals, critical by-products (gallium, scandium, rare earths), and advanced materials.

China’s National Stacked Model: A continent-spanning network of hundreds of massive, interconnected mega-kitchens operating in perfect symbiosis at the national scale.

Brazil’s Camaçari Model: A single, highly efficient master kitchen where 90+ specialist companies share one sophisticated central utility backbone for everything from power and water to waste recycling.

Pilbara Proposed Hub (Boodarie and linked Strategic Industrial Areas): A world-class Western refining kitchen already stocked with unmatched feedstock volumes, prime logistics, and accelerating renewable energy capacity, now deliberately installing the shared plumbing, benches, and coordination systems to unlock championship performance.

The table below compares the three models using identical metrics, including monetary values and energy availability. It shows where each hub stands today and where the Pilbara holds the clearest long-term advantage.

China leads in current scale and control; Camaçari demonstrates proven symbiosis in a non-superpower setting; and the Pilbara possesses unmatched feedstock volume, the strongest future green energy profile, and the governance transparency needed to capture the highest added value and market share once the shared commons are deliberately built.

1. China — The National Stacked Model (Multiple Massive Hubs)

China operates hundreds of specialised industrial parks and refining clusters across the country, with the largest 20–30 being true “mega-kitchens.”

Scale: Individual major clusters each represent US$10–50+ billion in cumulative infrastructure. The entire critical minerals refining system is national-scale.

Employment: Tens of thousands per major cluster; the overall sector employs hundreds of thousands in refining and related chemical processing.

Mineral stacking: In a single park, multiple feedstocks arrive and are processed in parallel circuits that feed each other. Bauxite is turned into alumina and gallium at the same site; copper concentrate produces metal plus tellurium and selenium from the same slimes; zinc gives indium and germanium; rare-earth concentrates are separated alongside all the above. Waste heat, reagents, and acids are shared.

Energy profile: Still heavily traditional (coal and hydro dominate many older parks), but China is adding renewable capacity at world-record speed. Many newer zones now have dedicated wind and solar farms supplying 30–60% of power.

Annual output/value: Controls 70–98% of global refining for dozens of critical minerals (98%+ gallium, 79% cobalt refining, dominant rare-earth separation). This is the architecture behind the $20–28 billion annual value leakage described in the first essay.

The competition = Baotou Rare-Earth Precinct, China: a city of 170,000 people entirely devoted to rare earths

2. Brazil — Camaçari (One Major Integrated Park)

A single, mature industrial park in Bahia that proves symbiosis works outside China.

Scale: One primary park with 90+ companies; total historical investment US$16 billion; annual revenue ~US$15 billion.

Employment: ~50,000 total jobs (10,000 direct + 40,000 indirect).

Mineral stacking: Feedstocks from multiple sources are brought in and processed together using shared utilities. The core is Cetrel — a central company that supplies water, treats all waste, recycles reagents, and manages pollution for every tenant. Recent additions (BYD EV factory, Windey battery plant, Brazilian Rare Earths separation) plug straight into the existing shared infrastructure.

Energy profile: Historically a traditional industrial mix, but rapidly greening. New tenants operate on 100% renewable electricity sourced from Bahia wind farms.

Annual output/value: >12 million tonnes per year of chemical and mineral products; responsible for 15% of Bahia’s exports and 22% of the state’s manufacturing GDP.

Cetrel

It’s useful to bookmark Cetrel’s structure because it seems well-evolved.

Cetrel (Central de Tratamento de Efluentes Líquidos) operates as the centralised environmental management and infrastructure provider for the Camaçari Industrial Complex (Polo Industrial de Camaçari) in Bahia, Brazil. Established in 1978 alongside the industrial park, Cetrel manages the ecological impact of more than 100 chemical, petrochemical, automotive, and manufacturing facilities within one of Latin America’s largest industrial hubs.

The organisation centralises environmental services, allowing individual industries to share a unified infrastructure grid for waste and water management. Its operations encompass several distinct areas:

Their latest venture is to place a BYD car factory in this same industrial zone so that ore can be taken to the end auto with minimal transport. Elon Musk has already completed a nickel and lithium refinery in the US, with an additional REE refinery being built for Tesla and SpaceX. These are two examples of the variety of vertical integration that is apparent.

Vertical integration is a trend to take note of. With increasingly complex supply chain risk, companies in many industries are looking for vertical local integration; it’s part of the deglobalisation impulse we are seeing.

From an Australian security perspective, we need to acknowledge that if Australia were, for some reason, cut off from Chinese refiners, we wouldn’t have adequate options for our ore in what would probably be a much higher-demand scenario.

Wastewater and Effluent Treatment: Cetrel operates the largest industrial effluent treatment plant in Latin America. It collects, neutralises, and treats complex liquid chemical waste generated by the park’s factories before safe discharge.

Water Supply and Reuse: The company supplies 100% of the demineralised, clarified, and potable water required by the complex, as well as the water network for the fire management system. It operates large-scale circular economy initiatives, such as the Água Viva project in partnership with Braskem, which treats and recycles billions of litres of wastewater and rainwater for industrial reuse.

Solid Waste Management: Cetrel executes the thermal disposal and incineration of hazardous industrial waste. It also operates zero-to-landfill projects, reverse logistics, and total waste management protocols for the industrial park.

Environmental Monitoring: The organisation maintains continuous surveillance of the region’s ecological health. This includes real-time air-quality monitoring stations, groundwater analysis to protect the underlying São Sebastião aquifer, and soil-contamination tracking.

Emergency Response: Cetrel provides the primary rapid-response teams for hazardous materials (HAZMAT) incidents, industrial fires, and chemical spills within the complex.

By centralising these utilities, Cetrel ensures continuous operational reliability and strict regulatory compliance for the entire industrial pole. Heavy industries operating in Camaçari rely completely on Cetrel’s shared infrastructure to sustain continuous production, integrating environmental protection mechanisms directly into the region’s manufacturing supply chain.

3. Pilbara (Proposed Multi-Mineral Hub — Boodarie & Linked SIAs)

The Pilbara already has the raw “ingredients” on a scale larger than either of the above; it is now assembling the shared kitchen.

Scale: Multiple Strategic Industrial Areas (Boodarie is the flagship, ~518 ha development envelope for the POSCO green iron project alone). Existing mining/processing infrastructure is world-scale; a full hub would anchor on hundreds of millions of tonnes of annual feedstock.

Employment: Existing iron ore operations already support tens of thousands of jobs; a mature multi-mineral hub could add thousands more direct, high-skill positions, plus indirect supply chain roles (conservative estimate: 8,000–15,000 total new jobs at full scale).

Mineral stacking: Currently siloed, but the policy direction is explicitly moving toward common-user design. Different streams would share power corridors, reagent supply, waste treatment, and logistics at Boodarie and linked sites.

Energy profile: The current grid is largely traditional/gas, but the Pilbara Energy Transition (PET) Plan and projects such as the Australian Renewable Energy Hub (AREH — up to 26 GW of wind + solar) and Fortescue’s 1.4+ GW solar + wind + battery network are transforming it. The proposed hub would operate under a “green overlay.”

Annual output/value: Anchor volume already exists (Rio + BHP >300 Mtpa iron ore equivalent plus critical minerals). A fully realised hub could realistically capture $4–11 billion recurring annual value for Western participants.

This is a Rio Tinto Gallium extraction unit located in Quebec that opened in May 2026

Key Takeaway for the Pilbara

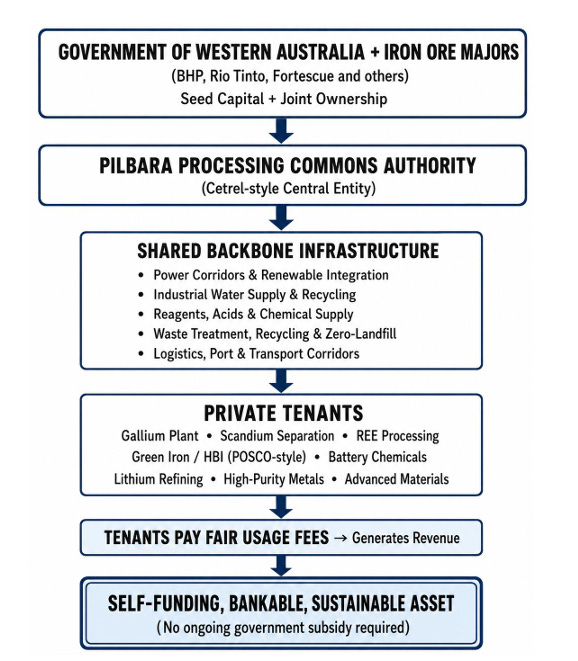

Both the Chinese and Brazilian parks succeeded for the same reason: a government, or a government-enabled body, took on the expensive shared layer — power, water, reagents, waste treatment — before any single tenant could justify it on its own. No private operator will fund infrastructure that its competitors also use, so the commons either gets built publicly or it doesn’t get built. That is the core function of the state here.

The Pilbara already has more feedstock and better renewable potential than either Camaçari or China’s parks had at the same stage. What it lacks is the funding and ownership structure for the commons. The practical model is a state-anchored entity, capitalised by government and the iron-ore majors who already operate here, that builds and owns the shared backbone and charges tenants a usage fee — the same Cetrel structure that already works in Brazil. This converts the commons from a cost no one will carry into an asset with a clear owner and a return. Settling who builds it, who owns it, and how tenants pay is the first decision; everything else waits on it.

The Pilbara already has more than sufficient volume to support a Brazil-like facility (or larger). A fully realised hub could realistically capture $4–11 billion recurring annual value for Western participants. It’s also a resilient model for Western Australia’s future; if we are going to do anything for future generations, tying this down is a worthwhile cause.

The Three Immediate Bottlenecks

While the Pilbara possesses the volume and the capital, executing a multi-mineral hub by 2030 requires confronting three immediate, pragmatic bottlenecks that could stall the transition:

The Labour and Housing Deficit:

A fully realised multi-mineral hub will require 8,000 to 15,000 new high-skill jobs. Western Australia currently faces a severe engineering deficit and a regional housing crisis. The transition requires a massive scale-up in entirely new disciplines, such as electrolyser engineering and green iron process chemistry. A new industrial ecosystem cannot be built in regional WA by simply importing skills from elsewhere; regional workforce development and housing accommodation must be built into the strategy from the start.

The Permitting Mathematical Trap:

A 2028 Final Investment Decision (FID) is impossible under the status quo, where navigating the Environmental Protection Authority (EPA) often takes three to five years. The state must weaponise the newly established Office of the Coordinator General (OCG) — an empowered entity whose explicit mandate is to drive project approvals, cut through coordination failures, and keep projects moving.

Aboriginal Equity as a Prerequisite:

In modern WA project finance, Indigenous equity partnerships are a prerequisite for land access and social license. The industry must commit to true partnership with Traditional Owners and regional communities. Integrating groups like the Kariyarra people at Boodarie, or learning from the Yindjibarndi Energy Corporation’s renewable projects, ensures that local capability, jobs, and ownership are foundational to the transition story.

The Eras of Western Australian State Development

Western Australia was never built by the market sitting back and waiting for an opportunity to appear.

It was built in waves. Each wave had a frontier. Each frontier needed the state to step in first, create the conditions for investment, and then let private capital do what it does best. That pattern runs through the whole history of WA.

The first frontier was settlement. The early state had to make a remote colony work: survey land, open roads, support ports, create towns and make basic economic life possible. Before there could be large private investment, there had to be access, order and infrastructure.

Then came gold. The goldfields pulled people and money inland, but discovery alone was not enough. Gold needed railways, water, towns, administration and ports. Geology created the opportunity. Infrastructure turned it into wealth.

Agriculture followed the same pattern. The state pushed settlement into the Wheatbelt and the South West through land schemes, soldier settlement and group settlement. Some of it worked. Some of it failed. That era matters because it shows both sides of state development: government can open a region, but it cannot ignore soil, water, debt and distance.

Kwinana marked the next turn. WA moved from opening land to the building industry. The state used land, infrastructure and State Agreements to attract heavy industrial projects. This was not passive government. It was active statecraft. The lesson was clear: big industry needs certainty, serviced land and a government willing to coordinate the hard parts.

The Pilbara iron ore era took that model to another scale. State Agreements unlocked remote ore bodies, ports, railways and company towns. It made modern WA rich. But it also created the weakness we are now trying to fix. The Pilbara model was brilliant at extraction. It was not designed for shared downstream processing. Companies, rail, ports, and supply chains worked to ship ore. They do not automatically create an industrial ecosystem.

Then came LNG. The North West Shelf and later gas projects showed that WA could host enormous, remote, technically difficult projects if the legal structure, offtake, infrastructure and capital were stitched together properly. These projects did not happen because the market casually solved everything. They happened because the architecture was built.

The China boom then pushed the extraction model to its peak. Iron ore, LNG, lithium and other commodities surged. WA became wealthier and more important to the global economy. But the boom also deepened the “dig and ship” habit. WA became exceptional at moving raw materials, while too much refining, chemical conversion, byproduct recovery, and advanced processing occurred elsewhere.

That is the problem now.

The next era cannot just be another mining boom. It has to be a processing era.

That means lithium chemicals, rare earth separation, green iron, battery materials, gallium recovery, mineral sands upgrading and the other messy but valuable steps that sit between the mine and the finished product.

This new era needs a different kind of infrastructure. Not just mines, rail and ports, but common-user power, transmission, reagents, waste treatment, water, industrial land, housing, skills and faster approvals. The Pilbara already has the scale, but the essay’s core point is that scale is not enough. The region needs shared architecture at Boodarie and linked Strategic Industrial Areas if it is going to become a real processing hub.

Why It Hasn’t Happened Already

The obvious question is why, if this value is real, private capital hasn’t already captured it. The answer is structural, not a matter of nerve. Each processing circuit, gallium recovery, scandium separation, and indium-germanium extraction, is uneconomic on its own when it must bear its full share of power, acid plants, water, and waste treatment. The value only appears when a dozen circuits share that backbone, and the fixed cost is spread across all of them.

But no single private operator will build infrastructure its competitors also use, and no one will commit to a circuit until the shared backbone already exists. Each rational actor waits for someone else to move first, so nothing moves. China didn’t out-compete the West here; it simply had a state willing to build the shared layer that unlocks every circuit at once. That is the precise gap a Pilbara commons fund is designed to close — not to subsidise industry, but to break the coordination deadlock that leaves billions in recoverable value stranded.

Conclusion

The Pilbara already has more than sufficient volume and renewable potential to support a world-leading facility. A fully realised hub could realistically capture $4–11 billion recurring annual value while creating thousands of high-skill jobs.

The immediate task is not to build every processing circuit at once. It is to establish the institutional vehicle that makes those circuits investable.

A Pilbara Processing Commons Authority, jointly capitalised by the Western Australian Government and foundation industry partners, with Traditional Owner equity participation built into its governance from the start. Its first mandate should be to scope, cost and finance the shared backbone: power corridors, industrial water, reagent supply, waste treatment, logistics access and environmental monitoring. Once that backbone has a clear owner, funding model and usage-fee structure, private tenants can invest in gallium recovery, scandium separation, rare-earth processing, green iron, battery chemicals and other high-value circuits without each project having to carry the full infrastructure burden alone.

More importantly, it would deliver a genuinely resilient industrial model for Western Australia’s future. If we are serious about building something worthwhile for future generations, tying down this processing commons is a cause worth pursuing with urgency.

The national security dimension makes the case compelling. In a world of increasing supply-chain fragility, relying on a single dominant foreign refiner for the “dirty middle” of our critical minerals chain is an unacceptable strategic risk.

Should access to Chinese capacity ever be curtailed, the enormous volumes of ore produced in Western Australia would suddenly have few reliable alternative destinations — precisely when global demand for processed critical materials would be at its peak. Australia cannot afford to remain exposed in this way. A sovereign Pilbara processing hub is therefore both an economic masterstroke and a national resilience necessity.

The skills of Australia (and indeed most western governments) today are firmly in applying layer after layer of regulatory interventions. The eyes of govt in Canberra will be lighting up with excitement with the number of state employees that will be required to regulate, inspect, scrutinise, etc. Folk lore has it that toward the end of the Vietnam war there were around 7 REMF’s for every combat soldier. Fear not Craig I have no doubt that between the State and central govt they can comfortably exceed this ratio of those working in the kitchens to state “supervisors”. We are dealing with energy and pollution, the favourite targets of your rapidly expanding govt. Let us not mention the interminable negotiations that will have to happen with the aboriginal peoples. The delicious irony of this is that China is supposed to be communist.

It's a long rant so buckle up.

I'm a bit confused about the reference to bauxite being processed in the pilbara. Afiak all the bauxite mined in wa is south east of perth and mostly refined locally at Alcoa and Worsley up to alumina oxide. Alcoa is looking at extracting the gallium with it looks like a bit of tax payer money probably because it's otherwise not commercially viable or because why not when someone else is paying. Worsley produce gallium as a by product since the 80s.

Boodarie although still in WA is literally half way to China from the darling range where bauxite is mined.

Port hedland predominantly ships iron ore typically 50-60% and most isnt refined before it's put into a blast furnace I doubt there are many by products from the slag. We have local steel makers, all seem to run on welfare. I suspect having a steel works in port hedland and karratha has been assessed and deemed not competitive by all major iron ore companies who'd otherwise have significant competitive advantage in this space.

There is some appreciable lithium tonnage going through port hedland too, you can read insights from them around whether it's viable to refine that past 6-8% locally. They also separate their byproducts and sell them..

Assuming ive missed something here and there is something potentially profitable to refine in the Pilbara locally that otherwise isnt. There are a number of other challenges to realizing the hubs you're talking about.

Energy is 1 of the largest costs of production in refining and despite what people tell you, you cannot run a 24/7 refinery on 'green' energy, nor is green energy green or particularly energetic, nor are we that good at producing it cheaply without murky accounting. No one who says this has costed a project. Those that do pass rely heavily on subsidies.

If you can run your plant steady and avoid significant loads starting and stopping or requiring significant reactive power and you have free land, 40% renewables is about where ROI starts to look very unpalatable. If you want to optimize for minimizing carbon and have a steady load and have had, then run a large ccgt - not a joke do the numbers.

Interestingly the swis, the energy grid both wa's alumina plants are connected to actually achieves renewable penetration close to these levels. Ignore that this requires pushing conventional generation to operate very inefficiently including switching off the steam gen on the ccgt on the grid.

The pilbara's cost of energy is higher than the swis and the actual publicly available grid is very limited. Every major miner runs their own private grids. China's costs are much lower as they use coal and have large well connected grids with lots of diversity. They run on a lot of Australian coal which makes you wonder why we don't burn it ourselves saving the energy to ship it and would support local refining and mamufacturing instead of worrying about what the best form of energy for us is. The short of it is we aren't having any energy intensive industries unless we embrace coal.

Areh's power when I last looked at it as an option to power a process plant was not remotely competitive and I suspect it will fade away.

Commodities are commodities. People generally don't care where it comes from which is how australians can hold virtuous green beliefs while simultaneously buying loads of plasticy stuff we don't need from china made from Russian and Iranian oil using coal power (some from Australia) and the DRCs cobalt.

Most importantly though as I suspect there'll be ideas about x byproduct from y at lower energy cost or green lmnop. China's attention span and desire to develop an economy at all costs is incomparable to Australians. They break ground while we're deciding who'll should get the butchers paper and who should do the invites for the stakeholder wishlist consultation. It's not even worth thinking about these things.

As a result I've concluded that the best future for Australia involves redrawing the Adelaide Brisbane line and letting the south east go.